With the Federal Reserve Open Market Committee (FOMC) decision to increase the Federal Funds Rate last week, the prospect of higher mortgage rates remains top of mind among real estate professionals and continues to generate headlines. Yet, changes to the short-term rate matter little to the housing market.

“The likely rise in mortgage rates is not the worry for first-time home buyers, but whether they can find something to buy in today’s supply-constrained market.”

It’s important to remember that mortgage rates, particularly the popular 30-year, fixed-rate mortgage, are benchmarked to the 10-year Treasury bond. While Federal Funds Rate hikes don’t directly drive up the yield on the 10-year Treasury, higher inflation expectations certainly do. The Fed’s decision to raise rates for the sixth time in a year and a half was primarily viewed by experts as a reaction to the possibility of higher inflation due to continued improvement in the labor market and economy in general.

Follow the 10-Year Treasury for a Read on Mortgage Rate Trends

Consider that, since the end of the recession, the 30-year, fixed-rate mortgage, on average, has stayed 1.7 percentage points higher than the 10-year Treasury bond yield. Today, the 10-year Treasury yield sits at 3 percent, which implies a mortgage rate of about 4.7 percent, given the trend since the end of the recession.

As long as economic fundamentals remain positive, it is reasonable to expect greater concern about inflation, which will likely influence the 10-Year Treasury to move higher and mortgage rates along with it. The Fed is also likely to increase the Federal Funds rate in response to inflationary concerns.

Outlook for Market Potential Amid Rising Mortgage Rates

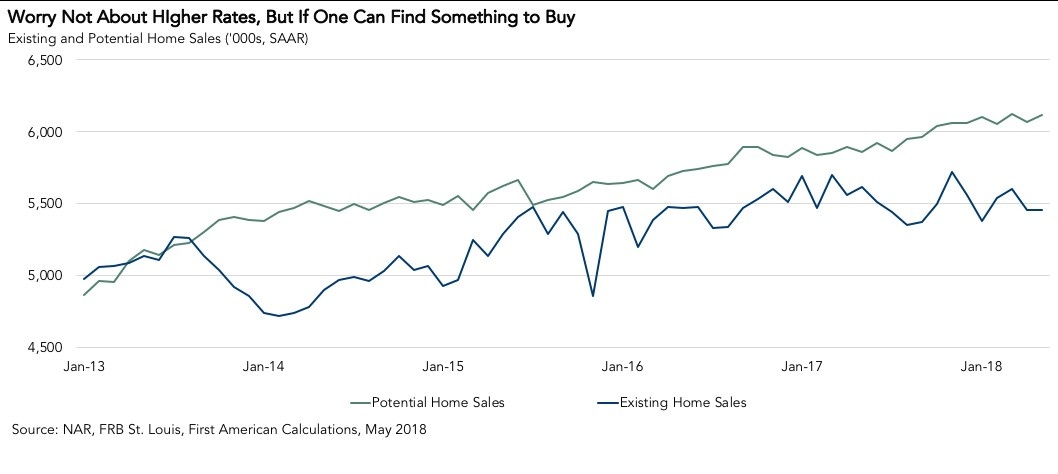

But, will higher mortgage rates curtail demand for housing? Our Potential Home Sales model estimates the market potential for existing-home sales based on market fundamentals, including the 30-year, fixed-rate mortgage rate. According to the model, the market potential for existing-home sales based on current fundamentals is 6.11 million at a seasonally adjusted annualized rate (SAAR). If the 30-year, fixed-rate mortgage rate increases to 5 percent, which most economists agree is likely by the end of 2018 or early 2019, the impact on the market potential would be a modest decline to 6.10 million existing-home sales, according to the model.

How does a rising mortgage-rate environment have so little impact on the pace of existing-home sales? The reason mortgage rates are rising – positive economic conditions – is also causing household income to rise, which helps offset the increase in borrowing costs from higher rates.

Additionally, home buyers can adjust to higher mortgage rates by substituting a lower rate adjustable-rate mortgage for the fixed-rate mortgage or buy a less expensive home. In other words, the housing market is flexible and can adjust to moderately higher mortgage rates without significant impact.

The likely rise in mortgage rates is not the worry for first-time home buyers, but whether they can find something to buy in today’s supply-constrained market.

May 2018 Potential Home Sales

For the month of May, First American updated its proprietary Potential Home Sales model to show that:

- Potential existing-home sales increased to a 6.11 million seasonally adjusted annualized rate (SAAR), a 0.8 percent month-over-month increase.

- This represents a 63.8 percent increase from the market potential low point reached in February 2011.

- The market potential for existing-home sales increased by 4.4 percent compared with a year ago, a gain of 255,100 (SAAR) sales.

- Currently, potential existing-home sales is 1.17 million (SAAR), or 16.1 percent below the pre-recession peak of market potential, which occurred in July 2005.

Market Performance Gap

- The market for existing-home sales is underperforming its potential by 4.7 percent or an estimated 289,000 (SAAR) sales.

- The market performance gap decreased by an estimated 36,000 (SAAR) sales between April 2018 and May 2018.

What Insight Does the Potential Home Sales Model Reveal?

When considering the right time to buy or sell a home, an important factor in the decision should be the market’s overall health, which is largely a function of supply and demand. Knowing how close the market is to a healthy level of activity can help consumers determine if it is a good time to buy or sell, and what might happen to the market in the future. That is difficult to assess when looking at the number of homes sold at a particular point in time without understanding the health of the market at that time. Historical context is critically important. Our potential home sales model measures what we believe a healthy market level of home sales should be based on the economic, demographic and housing market environments.

About the Potential Home Sales Model

Potential home sales measures existing-homes sales, which include single-family homes, townhomes, condominiums and co-ops on a seasonally adjusted annualized rate based on the historical relationship between existing-home sales and U.S. population demographic data, income and labor market conditions in the U.S. economy, price trends in the U.S. housing market, and conditions in the financial market. When the actual level of existing-home sales are significantly above potential home sales, the pace of turnover is not supported by market fundamentals and there is an increased likelihood of a market correction. Conversely, seasonally adjusted, annualized rates of actual existing-home sales below the level of potential existing-home sales indicate market turnover is underperforming the rate fundamentally supported by the current conditions. Actual seasonally adjusted annualized existing-home sales may exceed or fall short of the potential rate of sales for a variety of reasons, including non-traditional market conditions, policy constraints and market participant behavior. Recent potential home sale estimates are subject to revision in order to reflect the most up-to-date information available on the economy, housing market and financial conditions. The Potential Home Sales model is published prior to the National Association of Realtors’ Existing-Home Sales report each month.