Key Points:

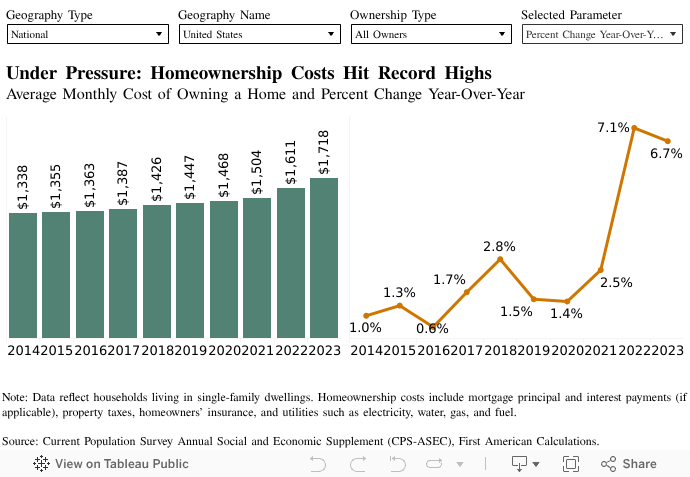

- The average monthly cost of owning a home in the U.S. soared to over $1,700 in 2023—a 17 percent increase from 2020—driven by across-the-board cost increases in mortgages, utilities, property taxes, and insurance.

- While mortgage holders face higher overall expenses, outright owners are seeing their housing budgets stretched more rapidly relative to income.

- Since 2020, both mortgage holders and outright owners have seen a gradual increase in the share of income going toward housing—pointing to a steady increase in pressure, not a sudden affordability crisis.

“While today’s homeownership costs as a share of income aren’t without historical precedent—similar to levels seen in 2018 for mortgage holders and 2015 for outright owners—the pace and scope of recent increases suggest the dream of homeownership is becoming harder to attain and sustain.”

The American dream of homeownership has long been a symbol of stability, wealth-building, and financial independence. But, in today’s market, that dream comes with a higher price tag. According to the latest Census data, the average monthly cost of owning a home in the U.S.—including mortgage payments, property taxes, insurance, and utilities—surpassed $1,700 in 2023, a 17percent increase since 2020 that amounts to $250 more per month. The steepest increases have hit mortgage borrowers, as rising interest rates and home prices have driven mortgage payments to record highs. Yet, even homeowners who’ve paid off their loans—often older adults on fixed incomes—are feeling the strain from rising taxes, insurance premiums, and utility bills. Whether trying to buy a home or simply stay put, more Americans are finding that the financial demands of homeownership are becoming harder to meet—and harder to manage.

Mortgage Holders and Outright Owners: Two Sides of the Cost Coin

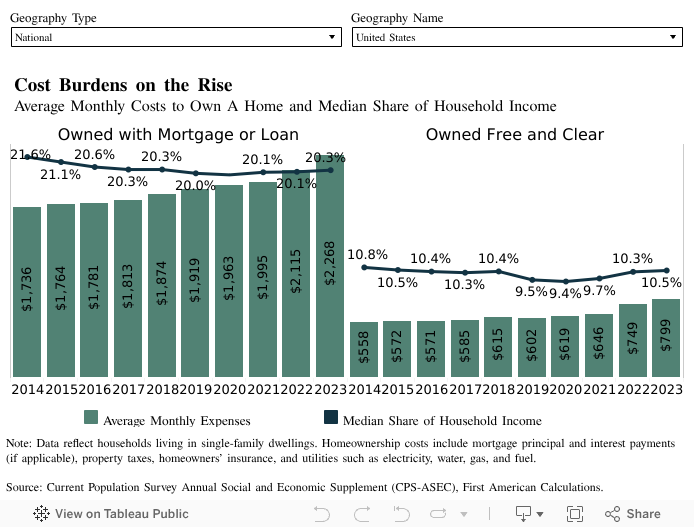

The increase in homeownership costs has impacted mortgage holders and outright owners—those who have paid off their mortgages and own their homes “free and clear”— differently. For borrowers, expenses have climbed more sharply in absolute terms (i.e., dollars), while for outright owners, the increases are steeper in relative (i.e., percentage) terms. From 2020 to 2023, for instance, mortgage holders saw their average monthly expenses rise by $305—a 16 percent increase— bringing their average monthly bill to an all-time high of $2,268. Monthly costs for outright owners, meanwhile, jumped almost twice as fast: increasing $180 per month, or 29 percent, to $799—another record high.

While both groups are paying more than ever to own their homes, the financial strain looks different depending on who is footing the bill. Mortgage holders, who tend to be younger and in their prime earning years, have done a better job offsetting rising costs with rising incomes. For this group, the median share of household income spent on homeownership hit a low of 19.8 percent in 2020 before edging up 0.5 percentage points to 20.3 percent in 2023. Outright owners, by contrast, are often older and more reliant on fixed incomes. Although their monthly costs remain lower in absolute terms, those costs have risen more sharply relative to income—pushing their housing burden up by 1.1 percentage points to 10.5 percent. Still, today’s affordability pressures aren’t without precedent: mortgage holders faced a similar burden rate as recently as 2018, and outright owners saw comparable levels back in 2015. So, while homeownership costs are rising, they’re not yet in unfamiliar territory.

Not All Homeowners Feel the Same Squeeze

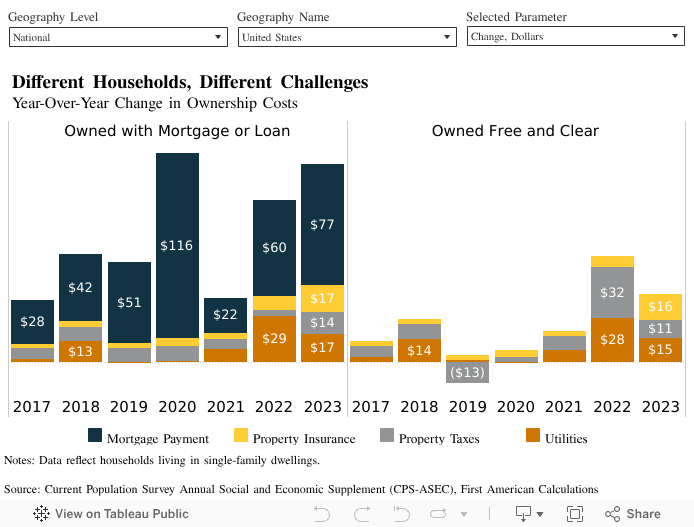

The increase in homeownership costs has impacted mortgage holders and outright owners—those who The source of rising housing costs isn’t one-size-fits-all—it depends on how the home is owned. For mortgage holders, the biggest cost pressure has come from monthly mortgage payments, their largest monthly expense. That burden grew in two waves. First, during the pandemic-fueled housing boom between 2019-2021 that limited supply and pushed prices to record highs. Then, as interest rates climbed sharply in 2022 and 2023, raising borrowing costs. Since 2019, the average monthly mortgage payment has increased by $275—a 22 percent jump that could add nearly $100,000 in additional payments over the life of a typical 30-year loan.

Even without mortgage payments, outright owners haven’t been spared from rising housing costs. Property taxes surged as pandemic-driven home value gains pushed up assessments—rising by $32 in 2022 and another $11 in 2023. That adds up to more than $500 in additional annual taxes, more than double the roughly $200 increase faced by mortgage holders over the same period. Both groups, however, saw similar increases in home insurance premiums, which have risen sharply since 2021, particularly in disaster-prone regions like the South—a trend that is likely to continue as extreme weather and climate disaster events increase in frequency and severity. Similarly, utility costs have risen for both groups, driven by electricity prices, which have continued to increase.

A Dream Under Pressure

While today’s homeownership costs as a share of income aren’t without historical precedent—similar to levels seen in 2018 for mortgage holders and 2015 for outright owners—the pace and scope of recent increases suggest the dream of homeownership is becoming harder to attain and sustain. With mortgage rates expected to remain elevated and insurance premiums anticipated to keep climbing in many regions, the key question is whether income growth can keep up—or whether more households will fall behind. In an upcoming analysis, we will examine the share of “cost burdened” households—those spending 30 percent or more of their income on housing costs—to uncover what cracks may lie beneath the headline figures and what they may signal for the future of housing affordability.