Key Points:

- Homeowners insurance premiums in the U.S. increased by 21 percent between 2021 and 2023, driven by severe weather-related events, rising construction costs, and higher claim payouts.

- The South, particularly coastal cities, faced the steepest hikes, with eight of the 10 metros with the fastest-growing premiums located in the region.

- Even as economic pressures ease, the impacts from severe weather-related events will continue to push premiums higher, challenging affordability for both new and existing homeowners.

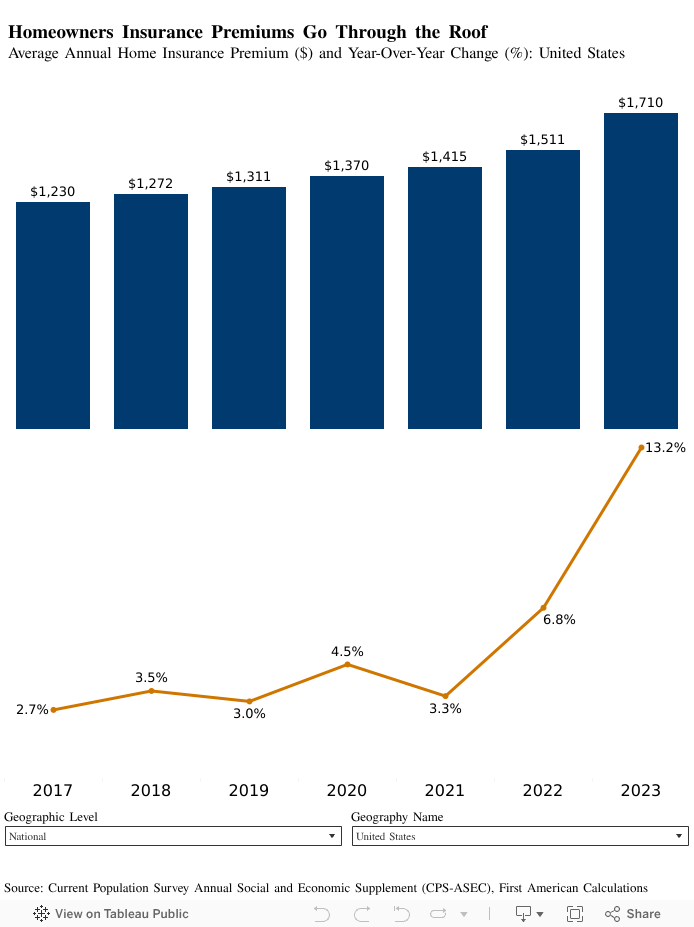

For most Americans, the family home is not just a place to live, but also their most significant financial asset. In recent years, however, the cost of insuring these valuable assets has surged. Between 2021 and 2023, U.S. homeowners’ insurance premiums jumped 21 percent—adding roughly $300 per policy each year—outpacing income growth and inflation while undermining the financial stability that homeownership provides. For prospective home buyers already grappling with affordability constraints from rising home prices and elevated interest rates, this additional expense further chokes their budgets and erodes their house-buying power. Meanwhile, existing homeowners, especially those on fixed incomes, face the risk of being unable to afford the very homes that once symbolized their financial stability.

“Between 2021 and 2023, U.S. homeowners insurance premiums jumped 21 percent—adding roughly $300 per policy each year—outpacing income growth and inflation, while undermining the financial stability that homeownership provides.”

As with all real estate matters, local dynamics play a crucial role in shaping market trends, and homeowners’ insurance is no exception. Our analysis of the latest 2023 data from the Census Population Survey Annual Social and Economic Supplement (CPS-ASEC) indicates that the surge in premiums is not uniform across the county. Instead, the surge has been concentrated primarily in the South, where premiums soared by an average of 25 percent between 2021 and 2023, adding roughly $425 per policy. Coastal cities, particularly those vulnerable to severe tropical storms and hurricanes, have been especially hard hit. In extreme cases, such as in New Orleans, premiums have skyrocketed a staggering 51 percent, highlighting how regional risk profiles are reshaping the cost of insurance.

Nature’s Fury and Economic Headwinds are Reshaping the Home Insurance Landscape

Homeowners insurance premiums are surging as a perfect storm of increased natural hazard risk and increased costs reshape the industry. At the heart of this trend is the increase in extreme weather and climate disaster events, both in frequency and severity. The National Oceanic and Atmospheric Administration (NOAA) estimates the annual number of billion-dollar disaster events has surged from 7 per year over the preceding four decades (1980–2019) to 23 per year over the past five years (2020–2024)—with 2023 and 2024 being the highest and second highest years on record at 28 and 27 events, respectively. At the same time, the annualized costs of these billion-dollar disasters have ballooned from approximately $55 billion to $151 billion. Additionally, reinsurance costs – that is, coverage that insurance companies take out to insure their own exposure – have increased, and these costs have been passed on to their own policy holders. Confronted with these mounting risks and costs, insurers are being forced to make the necessary adjustment to premiums for policy holders, particularly in these disaster-prone areas.

Although nature’s fury has undoubtedly pushed home insurance premiums skyward, escalating replacement and repair costs have played an equally significant role. Inflationary pressures have driven the cost of construction materials up by 35 percent from 2020 to 2023, with prices climbing an additional six percentage points through March, according to the latest Producer Price Index report. Meanwhile, persistent labor shortages have driven construction wages higher by nearly 26 percent over the same period, rising an additional six percentage points, as highlighted in the most recent Current Employment Statistics report. Insurers are expected to continue increasing premiums to offset these economic headwinds, though this this will vary by geography.

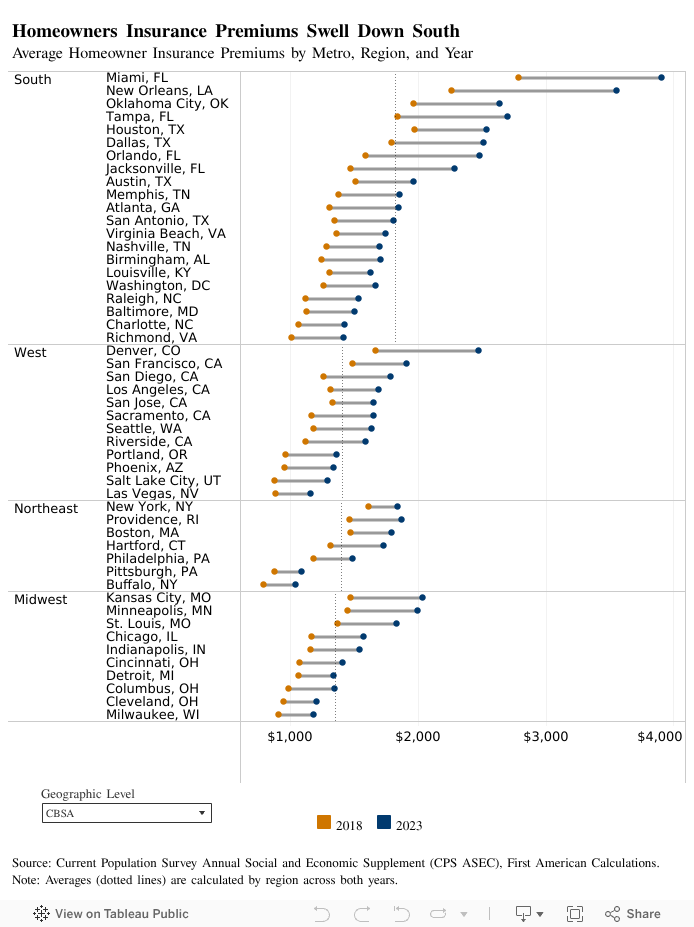

Southern Cities Bear the Biggest Brunt of Rising Premiums

Areas in the South prone to severe weather have borne the steepest increase in home insurance premiums. Among the nation’s 50 largest metro areas, eight of the 10 recording the most dramatic premium increases are in the South. In 2023, homeowners in this region shelled out an average of $2,120, significantly higher than the $1,575 paid elsewhere.

Coastal cities, where tropical storms and hurricanes loom large, have seen the sharpest increases. New Orleans tops the list, with a 51 percent increase in premiums from 2021 to 2023, translating into an extra cost of about $1,200 and pushing average annual premiums to more than $3,500. Elsewhere along the coast, premiums have increased in Jacksonville, Tampa, and Orlando by 38, 33, and 31 percent respectively from 2021 to 2023. Meanwhile, inland metros are also feeling growing financial pressures from severe storm events (i.e., tornado, hail, and high wind damage), with premiums in cities such as Birmingham, Ala.; Richmond, Va.; Atlanta; and Houston increasing 27, 25, 24, and 22 percent, respectively. With another 17 severe storms and five tropical storms recorded in 2024, additional price pressures loom over the Southern home insurance market, likely pushing premiums even higher.

Outside the South, Denver stands out as the sole metro where premium surges mirror those in the hardest-hit Southern markets. Premiums in the Mile High City have jumped 25.3 percent from 2021 to 2023, as increased wildfire and hail damage contribute to higher home insurance rates.

Severe Weather Events Will Continue Pushing Home Insurance Premiums

The surging cost of homeowners insurance presents a growing challenge to affordability, shaped by severe weather, economic pressures, and regional risk factors. With premiums expected to continue rising in many markets, particularly in disaster-prone regions like the South, the financial strain extends beyond prospective buyers struggling with high home prices and mortgage rates—it increasingly impacts established homeowners whose budgets are choked by mounting ownership costs. Looking ahead, we will conduct further analysis to explore how homeowners, both current and future, are weathering the storm of rising costs of homeownership around the country and the broader implications for housing affordability.