Key Points:

- For-sale inventory is up 9 percent year over year, and house-buying power has increased roughly 12 percent, easing some pressure on affordability.

- While overall inventory has improved, new listings are still down 4 percent from a year ago—limiting how much sales can rebound.

- Despite recent mortgage rate volatility and disappointing sales activity in January, pent-up demand and gradually improving supply conditions support a cautiously optimistic outlook.

Existing-home sales disappointed to start 2026, falling to the lowest level in more than a year. January’s decline raises understandable questions about the strength of the housing market as we head into the important spring home-buying season. Yet, as is often the case with early-year data, the story beneath the headline may be more nuanced.

Unusually cold temperatures and above-normal precipitation in parts of the country likely distorted January’s sales activity, making it more difficult than usual to assess the true underlying trend. Pending home sales data suggest that warmer, drier weather appears to have supported sales activity in the West, while weather-related headwinds weighed on the Northeast. As conditions normalize, some of that lost momentum in colder regions may re-emerge.

At the same time, geopolitical developments and shifting Treasury market dynamics generated some short-term volatility in mortgage rates. While mortgage rate fluctuations can affect buyer sentiment in the near term, geopolitical shocks tend to influence housing primarily through interest rates and confidence—not by fundamentally altering underlying demand. Heading into spring, the broader market fundamentals remain in better shape than a year ago.

“The housing market enters the spring season with a stronger foundation than a year ago.”

Why the Spring Home-Buying Season Outlook Remains Cautiously Optimistic

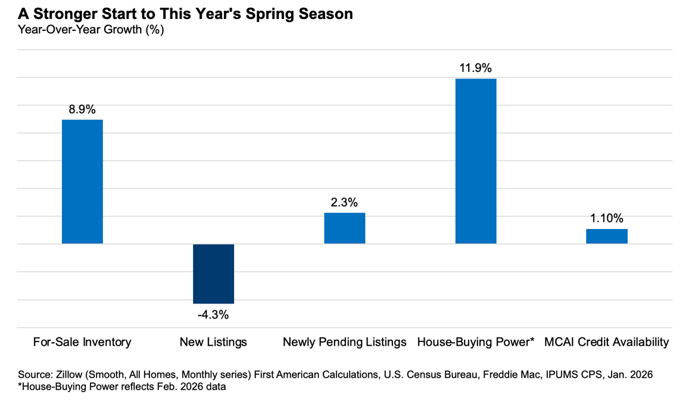

One of the most encouraging signals heading into the spring home-buying season is the improvement in for-sale inventory levels compared with last year. For-sale inventory in January was approximately 9 percent higher than a year ago—a meaningful shift in a market long defined by limited supply. More homes on the market give buyers greater choice and, combined with improved buying power, expand the range of homes they can realistically consider. After all, buyers can’t purchase what’s not for sale. A broader selection of available homes will typically fuel stronger sales activity.

Prospective home buyers will also benefit from improving house-buying power, which is up 12 percent compared with a year ago. While affordability remains stretched by historical standards, buyers today have more purchasing power than they did at this time last year. The sizeable year-over-year boost to house-buying power matters, particularly for buyers who were sidelined by last year’s combination of elevated mortgage rates and limited supply.

Newly pending listings from Zillow—listings that moved from for-sale to pending status—were up roughly 2 percent year over year in January. Because a shift to pending generally reflects a home going under contract, it offers an early read on near-term transaction momentum and closed sales in the months ahead. Credit availability, as measured by the MBA’s Mortgage Credit Availability Index (MCAI), has also modestly improved, rising just over 1 percent compared with a year ago. Looser credit conditions can help more qualified buyers access financing.

Together, these trends are incremental, but positive signals heading into the spring home-buying season. An uptick in new listings remains this missing ingredient to jumpstart the spring home-buying season. New listings were 4 percent lower than a year ago in January. Our research consistently shows that new listings are the lifeblood of the housing market. While rising for-sale inventory may reflect homes staying on the market slightly longer, it is new listings that drive sales volume. Without more homeowners deciding to sell, the market’s recovery will remain measured, rather than robust.

What Happens When Pent-Up Demand Meets Gradually Improving Supply?

Despite the sluggish start to the year, the housing market enters the spring season with a stronger foundation than a year ago. There remains significant pent-up demand from buyers who postponed their homeownership plans amid affordability challenges and limited options. The pent-up housing demand is not limited to potential first-time buyers. Many existing homeowners have also delayed moves despite life events—such as job changes, growing families, downsizing, or other transitions—that would typically prompt a home sale. Over time, those life-cycle needs accumulate, adding to the underlying demand for transactions on both the buy and sell side of the market.

The improvement in inventory and house-buying power suggests that conditions are gradually becoming more supportive of increased transaction activity. Of course, risks remain. Mortgage rates are likely to remain volatile, and affordability constraints have not disappeared. But housing demand is shaped primarily by demographics, labor market conditions, and life-cycle needs—forces that persist over time. As we move into the heart of the spring home-buying season, the key variable to watch is new listings activity. If more sellers step off the sidelines, existing-home sales could regain momentum as improving supply meets durable demand.

February 2026 Existing-Home Sales Outlook Highlights

For the month of February, First American updated its Existing-Home Sales Outlook Report to show that:

- Existing-home sales for February are expected to increase 0.9 percent from last month’s pace of sales, but remain 5 percent lower compared with the pace of sales a year ago.

- The largest contributors to the projected monthly increase in existing-home sales are a resilient economy (+0.5 percent), looser credit conditions (+0.09 percent), a weaker rate lock-in effect as measured by the lagged* spread between the prevailing market mortgage rate and the average rate for all outstanding mortgages (+0.09 percent), and rising house-buying power (+0.08 percent).

*The spread is incorporated with a two-month lag in the Existing-Home Sales Outlook model.

Methodology

Our Existing-Home Sales Outlook Report ‘nowcasts’ existing-home sales, which include single-family homes, townhomes, condominiums, and co-ops on a seasonally adjusted annualized rate based on the historical relationship between existing-home sales, U.S. demographic trends, house-buying power, and the prevailing financial and economic conditions, as well as momentum, a weight assigned to past values. Please note that the Existing-Home Sales Outlook Report is based on assumptions about demographic, economic and financial conditions. Actual values may differ from those projected. Recent existing-home sales estimates are subject to revision to reflect the most up-to-date information available on the economy, housing market and financial conditions.