Key Points:

- Markets with new listings nearer pre-pandemic norms generally have sales activity closer to those norms.

- Of the 75 metros tracked, 26 are “pace setters,” with both new listings and sales closer to their pre-pandemic averages than the typical market.

- The strong relationship between new listings normalization and sales volume normalization suggests that improving inventory is a key ingredient for a sustainable rebound.

After a long stretch of subdued activity, home sales remain sluggish, with the pace of sales still hovering near 4 million annualized. Our Existing-Home Sales Outlook points to a modest uptick in October because demand persists, but transactions have been constrained by limited supply and affordability challenges. One reason for cautious optimism is the modest improvement on the supply side. New listings have increased year over year and moved closer to pre-pandemic norms, easing one of the market’s most stubborn bottlenecks.

Why look back to pre-pandemic levels? The years before 2020 offers a reasonable benchmark for what ‘normal’ looked like—when demand, supply, and mortgage rates were more balanced. Comparing today’s housing market activity with that 2018–2019 period helps measure how far the market has recovered from the pandemic-era distortions —marked by a super sellers’ market, rate shocks, and surging prices—followed by the subsequent slowdown. The relationship is clearly positive: where new listings move closer to normal, sales tend to do so as well.

“This dynamic offers some optimism for 2026. As more homeowners list, more buyers will have opportunities to purchase, moving the market one step closer to balance. Where new listings grow, sales flow.”

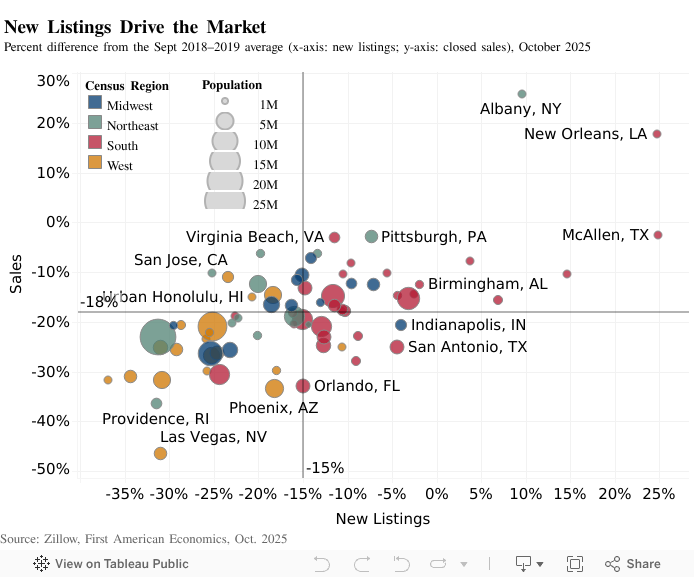

Four Quadrants of Normalization

To visualize that progress, we compare October 2025 new listings and sales in 75 major markets to each market’s own October 2018–2019 average—a simple ‘how close to normal’ check for both measures. We focus on new listings because flow matters for transactions. Active inventory can increase if homes take longer to sell, but new listings represent fresh supply that gives buyers real options. The result is a scatterplot divided into four quadrants, using the 75-market average for each measure as the midlines. With that framing, here’s what the quadrants show:

Pace setters (upper right: listings nearer normal, sales nearer normal)

These markets are closer to their own pre-pandemic October levels for both new listings and sales than they are for the typical market. These markets appear to be leading the return to more normalized activity as supply improves and sales respond. Examples include Pittsburgh, Knoxville, Tenn., and Virginia Beach, Va. This quadrant includes markets from the South, Northeast, and Midwest and many of these markets offer relative affordability.

Demand-ahead (upper left: listings lag, sales nearer normal)

Sales are closer to the market’s pre-pandemic norm than listings are — and closer than the typical market overall. Northeast and Midwestern markets dominate this quadrant. Think places like Detroit or Boston, where buyer appetite looks firm relative to what’s being listed. If supply loosens further, these metros could migrate into pace setters.

Supply-ahead (lower right: listings nearer normal, sales lag)

New listings have moved closer to normal than sales have—more so than the typical market. Many of these are Southern markets, such as Tampa, Fla. or San Antonio. The pattern likely reflects demand-side frictions: affordability constraints, rate sensitivity, or local economic and labor-market dynamics.

Stuck in neutral (lower left: listings lag, sales lag)

Both measures sit farther from each market’s pre-pandemic norm than the typical market. Western metros, such as Los Angeles and Portland, Ore., fall here—places where new listings remain below normal and sales have yet to catch up.

The Path Back to a Healthier Market

Looking ahead, this analysis offers a straightforward, but informative finding—new listings are an important factor in unlocking the housing market. They are not the only one—affordability, population growth, and local economic conditions matter—but markets that are closer to ’normal’ in listings are also closer to ‘normal’ in sales. This dynamic offers some optimism for 2026. As more homeowners list, more buyers will have opportunities to purchase, moving the market one step closer to balance. Where new listings grow, sales flow.

October 2025 Existing-Home Sales Outlook Highlights

For the month of October, First American updated its Existing-Home Sales Outlook Report to show that:

- Existing-home sales for October are expected to increase 0.3 percent from last month’s pace of sales, and increase 1.1 percent compared with the pace of sales a year ago.

- The largest contributors to the projected monthly increase in existing-home sales are a resilient economy (+0.3 percent), a weaker rate lock-in effect as measured by the lagged* spread between the prevailing market mortgage rate and the average rate for all outstanding mortgages (+0.3 percent), and higher house-buying power (+0.1 percent).

*The spread is incorporated with a two-month lag in the Existing-Home Sales Outlook model.

Methodology

Our Existing-Home Sales Outlook Report ‘nowcasts’ existing-home sales, which include single-family homes, townhomes, condominiums, and co-ops on a seasonally adjusted annualized rate based on the historical relationship between existing-home sales, U.S. demographic trends, house-buying power, and the prevailing financial and economic conditions, as well as momentum, a weight assigned to past values. Please note that the Existing-Home Sales Outlook Report is based on assumptions about demographic, economic and financial conditions. Actual values may differ from those projected. Recent existing-home sales estimates are subject to revision to reflect the most up-to-date information available on the economy, housing market and financial conditions.