Key Points:

- Housing cost burdens reached a new peak in 2023, with 16.9 million homeowners spending more than 30 percent of their income on housing—the highest level in over a decade.

- Nearly 60% of the increase in newly burdened homeowners since 2019 came from those spending over half their income on housing—showing that affordability challenges have grown more common and more severe.

- Cost-burdened younger and older homeowners have driven most of the increase since 2019, making up 87% of the three million newly affected households—highlighting growing pressure at both ends of the age spectrum.

“Since 2019, nearly nine in 10 newly cost-burdened homeowners have been either younger adults entering the market or seniors aging in place.”

For generations, homeownership has been a key pillar of financial stability—but that foundation is cracking for more Americans. With housing costs reaching historic highs, the number of cost-burdened homeowners has grown rapidly in the years following the pandemic. While affordability pressures are widespread, they are especially concentrated among those just starting out and those trying to remain in their homes later in life—highlighting growing challenges at both ends of the homeownership journey.

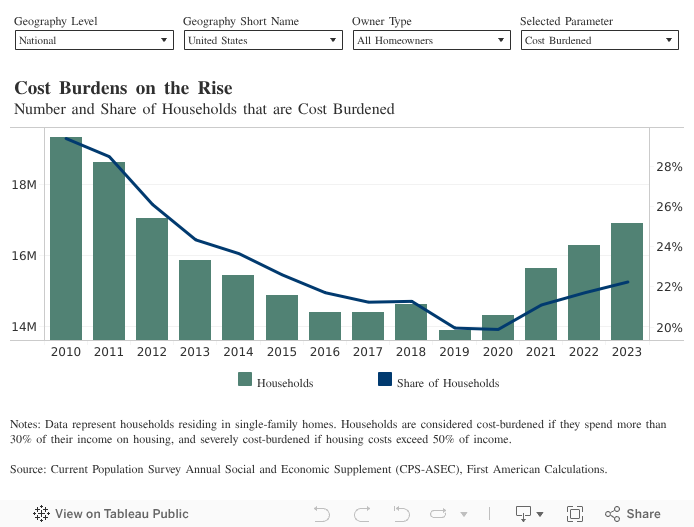

Affordability on the Backslide

While elevated home prices and mortgage rates are making it harder for new buyers to enter the market, rising expenses for taxes, insurance, and maintenance are placing added pressure on long-time homeowners. Together, these pressures have sent the number of cost-burdened households—defined as those spending more than 30 percent of their income on housing—soaring, increasing by three million between 2019 and 2023, a 22 percent leap. In 2023, the total number of cost-burdened homeowner households totaled 16.9 million, the highest level recorded since 2012. The share of homeowners with cost burdens also jumped to 22.2 percent, up 2.3 percentage points over four years.

It’s not just that more homeowners are struggling with housing costs—the severity of that struggle is also growing. Nearly six out of every 10 newly cost-burdened homeowners since 2019 are severely burdened, spending more than half their income on housing. In 2023, 7.3 million homeowners fell into this category—a 33 percent increase since 2019 and the highest level since 2011. The overall share of severely cost-burdened households now make up nearly one in 10 homeowners, reflecting the intensifying affordability challenges facing homeowners.

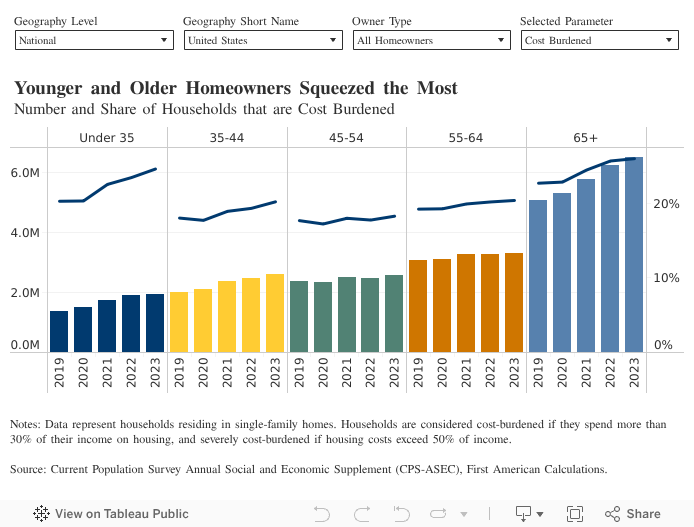

Struggling to Start, Struggling to Stay

While rising housing costs are affecting homeowners of all ages, the pressure is falling most heavily on those just getting started and those hoping to stay put later in life. Since 2019, nearly nine in 10 newly cost-burdened homeowners have been either younger adults or seniors aging in place. Homeowners 65 and older made up 47 percent of the increase, those between 35 and 44 added 20 percent, while those under 35 accounted for 18 percent. In contrast, middle-aged homeowners, those between 45 and 64, saw a much smaller increase, representing just 14 percent of the total.

Each age group faces its own set of challenges. For many senior homeowners, even though their mortgages are paid off, rising property taxes, insurance premiums, and utility bills are straining their fixed retirement incomes. Between 2019 and 2023, the number of cost-burdened homeowners aged 65 and older increased to 6.5 million—the highest level in over a decade. Today, more than one in four older homeowners spend over 30 percent of their income on housing, making it increasingly difficult for them to age in place and enjoy their golden years.

At the same time, younger homeowners are stretching their budgets to get their foot in the door amid unprecedented growth in home prices and elevated interest rates. Between 2019 and 2023, the number of cost-burdened homeowners under 35 increased by just over half a million—a 40 percent increase. Those aged 35 to 44 were not far behind, adding another 615,000—a 31 percent increase. In addition to rising housing costs, these younger households often carry higher levels of non-mortgage debt—such as student loans and credit card balances—compared to previous generations, making it harder to absorb unexpected expenses or accumulate wealth.

Middle-aged homeowners, in contrast, have fared better than their younger and older counterparts. The number of cost-burdened households between 45 and 64 rose by 332,000 from 2019 to 2023, an 8 percent increase. Many in this demographic are in their peak earning years, while also managing fewer financial obligations, such as student loans or credit card debt, and often having already paid off their mortgages. These combined factors place them in a financial sweet spot that helps them stay ahead of growing housing expenses more easily than other age groups. This widening gap underscores a growing divide: while younger and older homeowners feel the squeeze, those in the middle are, for now, holding relatively steady.

What Rising Burdens Could Mean for Tomorrow’s Market

The growing financial strain on younger and older homeowners in recent years highlights the challenges at both ends of the homeownership journey. Yet, while the data through 2023 paints a picture of rising burdens, there are signs of relief on the horizon. In today’s market, home prices are softening, incomes continue to grow, and mortgage rates are showing signs of stabilization—all of which could help ease some of the cost pressure that has accumulated. At the same time, rising costs for older homeowners may prompt more to downsize or move into assisted living—an often difficult decision, but one that could help free up much-needed housing in tight markets and improve affordability overall. Of course, age is just one part of the story—where people live matters, too. In an upcoming post, we’ll explore how housing affordability looks across different regions and what that means for homeowners navigating very different local markets.