The housing market outperformed its potential in May 2019. Actual existing-home sales are 0.2 percent above the market’s current potential, according to our Potential Home Sales model. Even as mortgage rates have decreased, and household income has increased, the market is underperforming compared to it’s potential from a year ago. What are the forces fueling the potential for existing-home sales in the market today?

“Yet, today, we are in an unprecedented homebody era, as many existing homeowners continue to feel rate-locked into their homes and seniors continue to age in place.”

In May, the 30-year, fixed mortgage rate, an important component of consumer house-buying power, fell to its lowest point since January 2018, and declined 0.07 percentage points compared to the previous month. Lower mortgage rates help to increase consumer house-buying power. Household income, the other main component of consumer house-buying power, continued to rise, increasing 2.6 percent compared with one year ago. The combination of lower mortgage rates and rising household income triggered a surge in house-buying power that propelled the housing market to outperform its potential this month. Despite the stronger performance, potential home sales remain nearly 80,000 units below the level of a year ago.

Forces Fueling Market Potential

Since last year, several forces have helped increase the market potential for existing-home sales. House-buying power, driven by falling mortgage rates and rising household income, contributed to a gain of 183,000 potential home sales compared with one year ago. Compared with May 2018, rising house prices also contributed positively, increasing the market potential for home sales by 41,000.

Additionally, loosening credit standards boosted the marketing potential for home sales by more than 60,000 sales over the last year. Some modest growth in new-home construction also added 1,000 potential home sales. Finally, the growth in household formation, as millennials continue to form households, contributed nearly 81,000 potential home sales compared with a year ago. Despite all the positives, the market potential for home sales remains nearly 80,000 units below the level of a year ago.

Unprecedented Homebody Era is Here

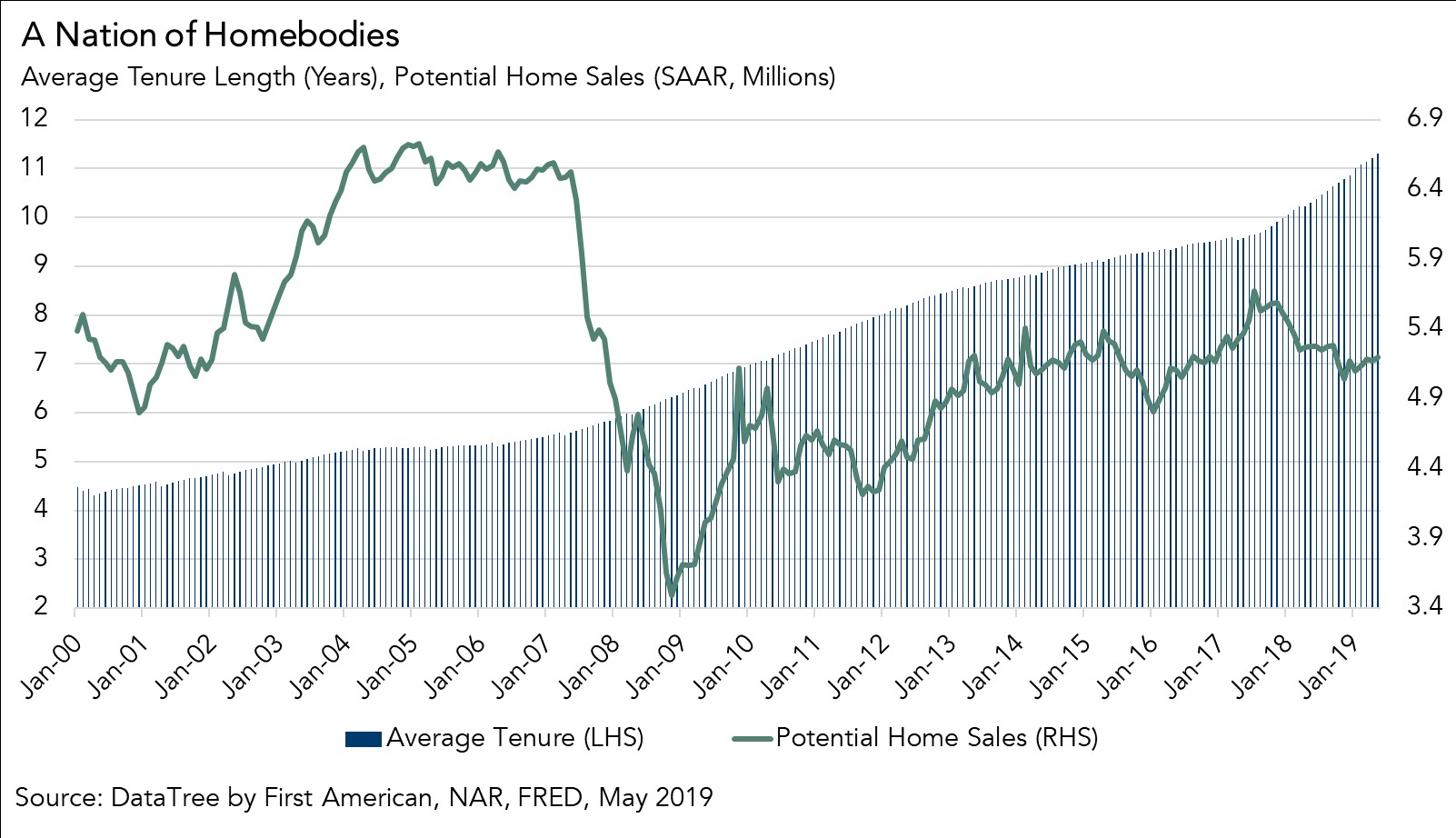

Collectively, the aforementioned market forces contributed to a positive gain of 366,000 potential home sales, but it was not enough to offset the loss of 446,000 potential sales due to the impact of rising tenure. The average tenure length, the amount of time a typical homeowner lives in their home, has increased dramatically in the last year. Since existing homeowners supply the majority of the homes for sale and increasing tenure length indicates homeowners are not selling, the housing market faces an ongoing supply shortage – you can’t buy what’s not for sale.

Before the housing market crash in 2007, the average length of time someone lived in their home was approximately five years. Average tenure length jumped to seven years during the aftermath of the housing market crisis between 2008 and 2016. The most recent data shows that the average length of time someone lives in their home reached 11.3 years in May 2019, a 10 percent increase compared with a year ago.

Two trends are driving the increase in tenure length. The majority of existing homeowners have mortgages with historically low rates, so there is limited incentive to sell if it will cost them more each month to borrow the same amount of money from the bank. While mortgage rates have come down compared with last year, they are still below the 3.5 percent mortgage rates of 2016.

The second trend influencing tenure is seniors aging in place. A recent study from Freddie Mac shows that if seniors and adults born between 1931-1959 behaved like earlier generations, nearly 1.6 million housing units would have come to market by 2018. Improvements in health care and technology have made ageing in place easier, which has meant fewer homes on the market.

So far in 2019, the market potential for existing-home sales has benefitted from lower mortgage rates and rising household income, all contributing to stronger house-buying power. Surging consumer house-buying power coupled with rising household formation has resulted in strong demand for homes.

Yet, today, we are in an unprecedented homebody era, as many existing homeowners continue to feel rate-locked into their homes and seniors continue to age in place. Looking ahead, more than half of all existing-homes are owned by baby boomers and the silent generation and they will eventually age out of homeownership. But right now, housing supply remains tight – you can’t buy what’s not sale -- and market potential is lower because of it.

May 2019 Potential Home Sales

For the month of May, First American updated its proprietary Potential Home Sales Model to show that:

- Potential existing-home sales increased marginally to a 5.20 million seasonally adjusted annualized rate (SAAR), a 0.4 percent month-over-month increase.

- This represents a 54.8 percent increase from the market potential low point reached in February 1993.

- The market potential for existing-home sales declined by 1.5 percent compared with a year ago, a loss of 79,500 (SAAR) sales.

- Currently, potential existing-home sales is 1.53 million (SAAR), or 22.7 percent below the pre-recession peak of market potential, which occurred in March 2004.

Market Performance Gap

- The market for existing-home sales is outperforming its potential by 0.2 percent or an estimated 11,400 (SAAR) sales.

- The market performance gap decreased by an estimated 2,670 (SAAR) sales between April 2019 and May 2019.

First American Deputy Chief Economist Odeta Kushi contributed to this post.

What Insight Does the Potential Home Sales Model Reveal?

When considering the right time to buy or sell a home, an important factor in the decision should be the market’s overall health, which is largely a function of supply and demand. Knowing how close the market is to a healthy level of activity can help consumers determine if it is a good time to buy or sell, and what might happen to the market in the future. That is difficult to assess when looking at the number of homes sold at a particular point in time without understanding the health of the market at that time. Historical context is critically important. Our potential home sales model measures what we believe a healthy market level of home sales should be based on the economic, demographic and housing market environments.

About the Potential Home Sales Model

Potential home sales measures existing-homes sales, which include single-family homes, townhomes, condominiums and co-ops on a seasonally adjusted annualized rate based on the historical relationship between existing-home sales and U.S. population demographic data, homeowner tenure, house-buying power in the U.S. economy, price trends in the U.S. housing market, and conditions in the financial market. When the actual level of existing-home sales are significantly above potential home sales, the pace of turnover is not supported by market fundamentals and there is an increased likelihood of a market correction. Conversely, seasonally adjusted, annualized rates of actual existing-home sales below the level of potential existing-home sales indicate market turnover is underperforming the rate fundamentally supported by the current conditions. Actual seasonally adjusted annualized existing-home sales may exceed or fall short of the potential rate of sales for a variety of reasons, including non-traditional market conditions, policy constraints and market participant behavior. Recent potential home sale estimates are subject to revision to reflect the most up-to-date information available on the economy, housing market and financial conditions. The Potential Home Sales model is published prior to the National Association of Realtors’ Existing-Home Sales report each month.

.jpg)