Key Points:

- National housing affordability rose 3.1 percent year over year in June, marking the fifth consecutive month with an annual gain.

- Prices are decelerating or declining in many markets, boosting affordability, though pandemic-era equity gains remain largely intact.

- Affordability will likely improve slowly as income growth outpaces house price growth, inventory rises, and mortgage rates ease, signaling a gradual shift in favor of buyers.

Housing affordability across the nation improved by 3.1 percent year over year in June, marking the fifth consecutive annual gain. Falling mortgage rates, slowing nominal house price growth, and rising household incomes drove the improvement. Preliminary data from July and August suggests the trend likely has continued, pushing affordability to levels last seen in September 2024—a nearly 12 percent improvement from the low point in October 2023. While affordability, as measured by the Real House Price Index (RHPI), remains more than 70 percent higher (worse) than the pre-pandemic five-year average, the recent rebound is an encouraging sign for potential buyers.

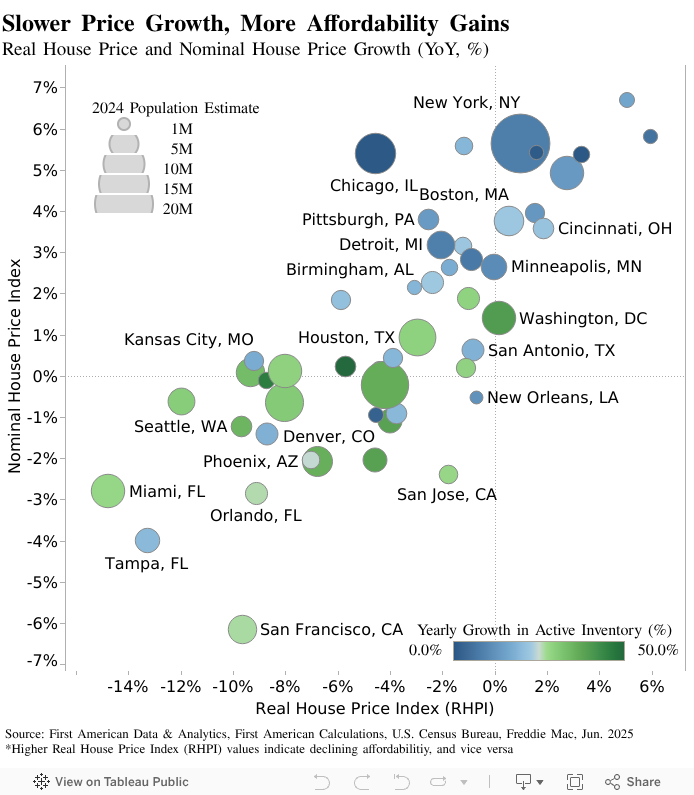

A key driver of improving affordability is the slowdown in house price growth. In June, prices declined or grew less than 1 percent annually in 27 of the 50 markets we track, and income growth outpaced home price appreciation in 35 of the 50 markets. San Francisco led in price declines with a nearly 6 percent year-over-year drop, while Louisville, Ky., posted a 7 percent annual increase. In both markets, household incomes rose on annual basis, further boosting affordability in San Francisco and helping to offset the impact of rising prices in Louisville. While sellers may feel the pinch of waning pricing power, slower price growth—paired with rising incomes—is finally giving buyers a much-needed edge.

“For prospective buyers who have been waiting on the sidelines, the housing market is finally starting to listen.”

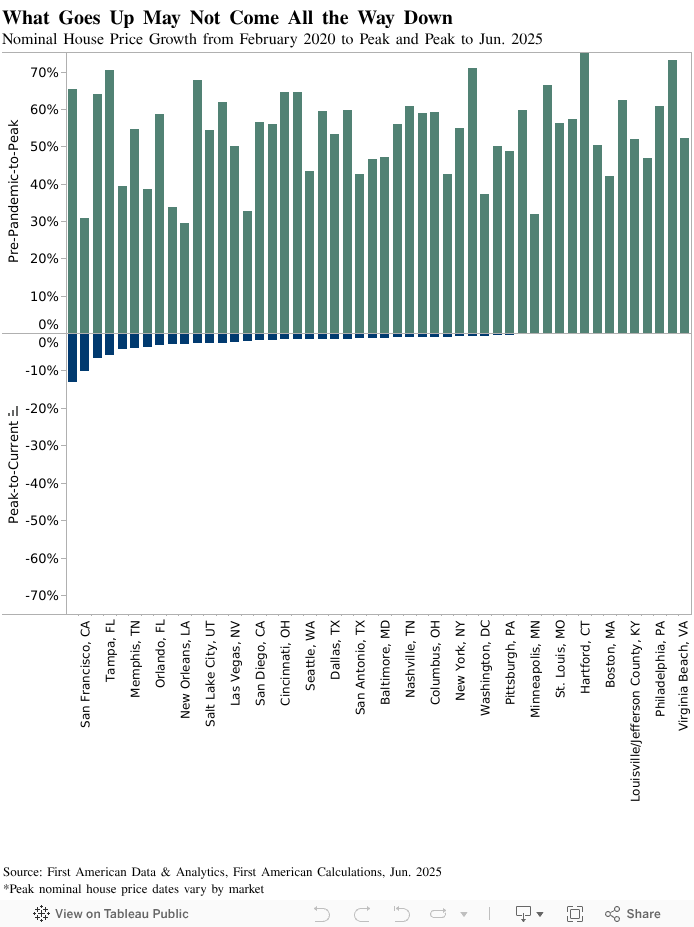

What Do Declining Prices Mean for Sellers?

For sellers, especially those who bought before or during the pandemic boom, it’s not all bad news. As of June, prices have fallen below their peaks in 42 of the top 50 markets we track. Austin, Texas, has seen the steepest decline, with prices down 13 percent from its June 2022 peak. San Francisco follows closely, with a 10 percent drop since its April 2022 peak. However, context matters. Even with these declines, much of the pandemic-era price appreciation remains intact. In Austin, prices surged 65 percent from February 2020 to June 2022. In San Francisco, they climbed 31 percent over roughly the same period. In short, it would take a substantial and sustained downturn to erase the equity gains homeowners have built over the past few years.

What’s the Outlook for Buyers?

Price deceleration—or outright declines—translates into improved affordability for buyers. In fact, affordability improved in 39 of the 50 markets we track on an annual basis in June. Affordability improved the most in markets like San Francisco, where prices are falling. Conversely, affordability is eroding in markets such as Philadelphia, where prices continue to climb. Another trend worth noting is that markets with downward price pressure often have strong growth in active inventory. More inventory means more competition among sellers, which often leads to price cuts and greater buyer bargaining power—a recipe for improved affordability.

Slow and Steady Improvements in Affordability to Come

Affordability is beginning to shift—gradually and unevenly—but the momentum is turning. The most likely path forward is a slow rebalancing, driven by income growth outpacing home price appreciation, some moderation in prices as inventory improves, and eventual downward pressure on mortgage rates, if economic conditions soften. While this process will take time, likely years, the balance of power is no longer as one-sided as it was during the pandemic frenzy. For those prospective buyers who have been waiting on the sidelines, the housing market is finally starting to listen.

Sources:

• First American Data & Analytics

• Freddie Mac

• Census Bureau

June 2025 Real House Price Index Highlights

The First American Data & Analytics’ Real House Price Index (RHPI) showed that in June 2025:

- Real house prices decreased 3.1 percent between June 2024 and June 2025.

- Real house prices decreased 0.1 percent between May 2025 and June 2025.

- Consumer house-buying power, how much one can buy based on changes in income and mortgage rates, increased 0.2 percent between May 2025 and June 2025, and increased 5.1 percent year over year.

- Median household income has increased 4.0 percent since June 2024 and 58.1 percent since January 2015.

- Real house prices are 33.9 percent more expensive than in January 2000.

- Unadjusted house prices are now 63.8 percent above the housing boom peak in 2006, while real, house-buying power-adjusted house prices are 6.2 percent below their 2006 housing boom peak.

June 2025 Real House Price State Highlights

- The five states with the greatest year-over-year increase in the RHPI are: South Dakota (+7.4 percent), Maine (+5.8 percent), New Hampshire (+4.6 percent), Connecticut (+3.0 percent), and Alaska (+2.7 percent).

- The five states with the greatest year-over-year decrease in the RHPI are: Florida (-10.5 percent), Montana (-9.2 percent), Wyoming (-7.5 percent), Nevada (-7.5 percent), and Texas (-7.3 percent).

June 2025 Real House Price Local Market Highlights

- Among the Core Based Statistical Areas (CBSAs) tracked by First American Data & Analytics, the five markets with the greatest year-over-year increase in the RHPI are: Hartford, Conn. (+5.9 percent), Louisville, Ky. (+5.1 percent), Milwaukee (+3.3 percent), Philadelphia (+2.8 percent), and Cincinnati (+1.9 percent).

- Among the Core Based Statistical Areas (CBSAs) tracked by First American Data & Analytics, the five markets with the greatest year-over-year decrease in the RHPI are: Miami (-14.8 percent), Tampa, Fla. (-13.3 percent), Seattle (-11.9 percent), Sacramento, Calif. (-9.7 percent), and San Francisco (-9.7 percent).

Next Release

The next release of the First American Data & Analytics’ Real House Price Index will take place the week of September 22, 2025.

About the First American Data & Analytics’ Real House Price Index

The traditional perspective on house prices is fixated on the actual prices and the changes in those prices, which overlooks what matters to potential buyers - their purchasing power, or how much they can afford to buy. First American Data & Analytics’ proprietary Real House Price Index (RHPI) adjusts prices for purchasing power by considering how income levels and interest rates influence the amount one can borrow.

The RHPI uses a weighted repeat-sales house price index that measures the price movements of single-family residential properties by time and across geographies, adjusted for the influence of income and interest rate changes on consumer house-buying power. The index is set to equal 100 in January 2000. Changing incomes and interest rates either increase or decrease consumer house-buying power. When incomes rise and mortgage rates fall, consumer house-buying power increases, acting as a deflator of increases in the house price level. For example, if the house price index increases by three percent, but the combination of rising incomes and falling mortgage rates increase consumer buying power over the same period by two percent, then the Real House Price index only increases by 1 percent. The Real House Price Index reflects changes in house prices, but also accounts for changes in consumer house-buying power.

Disclaimer

Opinions, estimates, forecasts and other views contained in this page are those of First American’s Chief Economist, do not necessarily represent the views of First American or its management, should not be construed as indicating First American’s business prospects or expected results, and are subject to change without notice. Although the First American Economics team attempts to provide reliable, useful information, it does not guarantee that the information is accurate, current or suitable for any particular purpose. © 2025 by First American. Information from this page may be used with proper attribution.