In January of 2013, the mortgage industry witnessed the birth of a new income-underwriting era. The Consumer Finance Protection Bureau (CFPB) published new requirements for mortgage lenders to carefully assess a consumer’s ability to repay their mortgage loan. The new standards were dubbed the “ability-to-repay” rules and were set to take effect one year later in January 2014.

"The ancillary benefit (of the ability-to-repay standards) has been fewer loan application defects and a ‘steering wheel lock’ on mortgage fraud risk."

The “ability-to-repay” rules were intended to discourage the use of high-risk stated income loans that were common during the housing boom. The new rules also required lenders to strengthen the mortgage loan manufacturing and underwriting practices associated with the determination of a consumer’s ability to repay. But, what impact did the ability-to-repay rules have on loan application misrepresentation, defect and fraud risk?

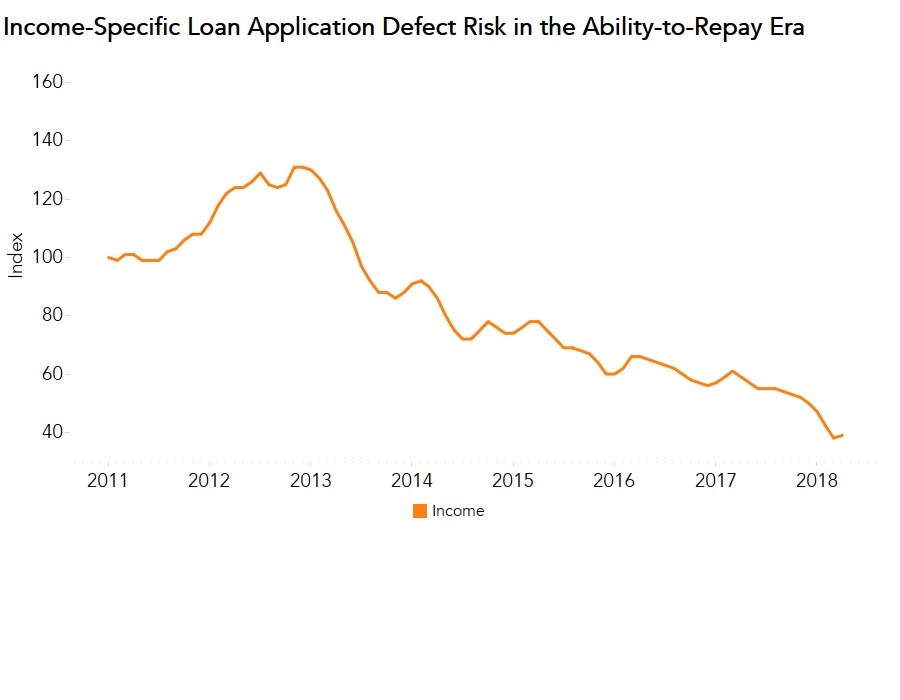

Income-Specific Loan App Defect Risk Crashes Since December 2012

Since the ability-to-repay rules were issued, there has been a precipitous and significant decline in income-specific mortgage loan application misrepresentation, defect and fraud risk. In fact, our income-specific metric within the Loan Application Defect Index (LADI) reached its peak in December 2012, one month before the rules were issued. By September 2013, nine months later, the income-specific defect risk metric declined 33 percent, as lenders implemented new loan manufacturing and underwriting practices in preparation for the effective start of rule in January 2014. Since then, income-specific defect and fraud risk has continued to decline and is currently 70 percent below its peak prior to publication of the ability-to-repay rules.

The ability-to-repay standards require mortgage lenders to make a reasonable and good faith determination of the consumer’s ability to repay their mortgage. The rules have reduced the incentive to fraudulently misrepresent one’s income, a benefit to lenders. The ability-to-repay standards are essentially the mortgage fraud risk prevention equivalent of using a steering wheel lock to dissuade potential car thieves.

The Mortgage Fraud Risk Prevention Equivalent of a Steering Wheel Lock

Additionally, in order to make the good faith determination, the mortgage industry enhanced the manufacturing and underwriting practices specific to the assessment of a consumer’s income and ability to repay their mortgage. This has helped to reduce income-related loan application defects.

The intent of the ability-to-repay standards was to help consumers secure mortgages that they can reasonably expect to repay. The ancillary benefit has been fewer loan application defects, and a steering wheel lock on mortgage fraud risk.

For Mark’s full analysis on loan defect risk, the top five states and markets with the greatest increases and decreases in defect risk, and more, please visit the Loan Application Defect Index.

The Defect Index is updated monthly with new data. Look for the next edition of the Defect Index the week of June 25, 2018.