Contrary to many reports, student loan debt is not an insurmountable barrier to homeownership for millennials. Student loan debt is more likely to delay the timing of homeownership, but it does not necessarily prevent homeownership. But, this begs the questions, how does student loan debt impact house-buying power? And, is higher education a worthwhile investment?

“Student loan debt adds up, but higher education leads to higher income, and the increase in income attributable to higher education far outweighs the impact of student loan debt.”

Student Loans and House-Buying Power

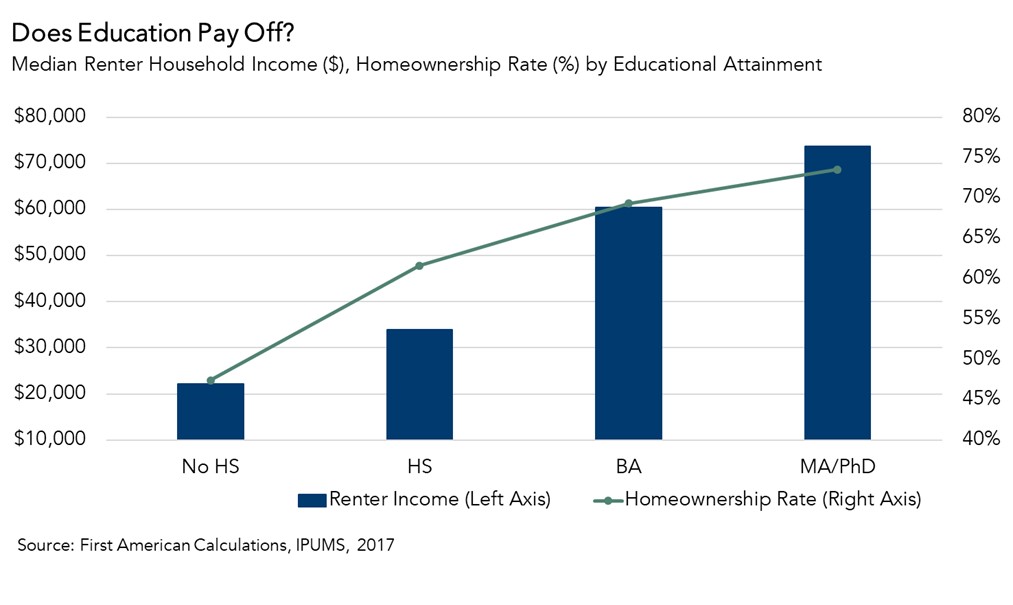

To examine the impact of student loan debt on house-buying power, we first look at the median household income of a prospective first-time home buyer, who is, by definition, a renter. When breaking down the most recent median income data available (2017) by educational attainment, we find that renter household income increases as educational attainment increases: no high school degree ($22,146), high school degree ($33,870), bachelor’s degree ($60,373), and graduate level education ($73,710).

Using this median income data, we can calculate how much home one can afford to buy at each level of educational attainment. A renter’s house-buying power is based on the prevailing 30-year, fixed mortgage rate (4.64 percent in January), and assumes a 5 percent down payment and that one-third of pre-tax income is used for the mortgage. Using this calculation, renter house-buying power at each education level is:

- No high school education: $127,123

- High school education: $194,415

- Bachelor’s degree: $346,540

- Graduate level (MA and/or PhD): $423,096

The average student loan debt for those that complete their bachelor’s degree is approximately $30,000. Assuming a 6 percent Federal direct student loan interest rate means the average monthly payment is just above $300 per month, or nearly $4,000 per year. This reduces median household income for those that complete their bachelor’s degree and, therefore, reduces house-buying power by $23,000 to $323,603. While the reduction in house-buying power is not ideal, renter house-buying power for those with a bachelor’s degree is still more than $120,000 greater than renters with just a high school education. So, can student loans ever repay you? It looks like they can, in the form of greater income and higher house-buying power.

Homeownership is Higher Too

While higher education leads to higher house-buying power, does this positively influence home buying? Based on the latest available household census data in 2017, homeownership rates for those with a bachelor’s degree are nearly 8 percent higher than those with a high school degree. This difference becomes more exaggerated when comparing those with a college degree to those who do not complete high school, nearly a 25 percent difference in homeownership rates.

Education Pays Off

It is no secret why millennials are waiting to buy homes until after they have attained their educational goals, because education pays off. Overall, 9 out of 10 millennials say their college education was worthwhile and have already paid off their debt or will in the future. Student-debt adds up, but higher education leads to higher income, and the increase in income attributable to higher education far outweighs the impact of student loan debt. Although the price of college may seem intimidating, the cost of not going to college—in the long run—may be worse.