The early signs of a housing market comeback that appeared in mid-April, rising weekly purchase loan applications, continued to surge through May and into June. In fact, weekly purchase loan applications have now exceeded pre-pandemic levels.

While the coronavirus pandemic continued to negatively impact the domestic and global economy in May, the market potential for existing-home sales rebounded from the April low point, according to our Potential Home Sales Model. In May, housing market potential increased to 4.92 million SAAR, a 6 percent improvement compared with April, but remained 7 percent lower than one year ago. The two biggest drivers of the increase in May are slightly loosening credit standards, which allow more potential home buyers to qualify for financing, and the increase in house-buying power due to historically low mortgage rates.

“Record low mortgage rates are proving to be a powerful motivator and benefit for home buyers in an otherwise challenging time.”

The increase in house-buying power is also a major reason why market potential is not even lower compared with one year ago. During economic downturns, the housing market benefits in one specific way – monetary policy is usually eased to boost the economy, often leading to falling mortgage rates, which increases consumer house-buying power and makes homes more affordable. Relative to one year ago, the potential for existing-home sales declined by 368,120 (SAAR), but it could’ve been worse were it not for the house-buying power boost from low mortgage rates.

Tight Credit Standards, Limited Supply Dampen Housing Market Potential

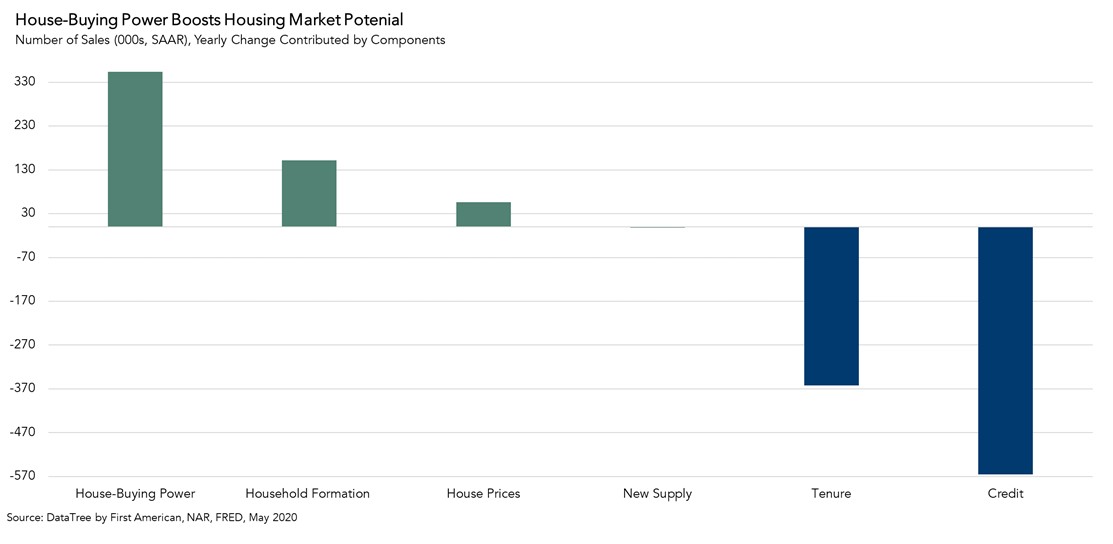

In May, there were several forces holding back the market potential for existing-home sales. Lenders have tightened their lending criteria to account for the greater likelihood of forbearance and delinquency. Even though lenders eased credit standards slightly in May compared with April, tightening credit still had the largest year-over-year negative impact (565,340 potential home sales) on potential home sales. Additionally, increasing tenure length means fewer homes for sale, further limiting housing supply and reducing housing market potential by 362,440 sales. The supply of new homes for sale also fell relative to one year ago, further reducing the ability to find something to buy, and thereby holding back potential by 1,916 sales.

Low Mortgage Rates Buoy Housing Market Potential

Given these headwinds, the market potential for existing-home sales could have declined by nearly 930,000 sales. Yet, the 30-year, fixed-rate mortgage fell to its lowest level in nearly 50 years in May, boosting house-buying power by 15.3 percent relative to one year ago. The increase in house-buying power resulted in a 354,000 increase in potential home sales, helping offset some of the impact from the credit and housing supply headwinds. Additionally, millennials continue to form new households amid the pandemic, which boosted demand for housing by 152,000 sales. Finally, the continued growth in house price appreciation, which is the result of rising demand against limited supply of homes for sale, positively contributed to potential home sales in May relative to one year ago by 56,000 sales. As a homeowner gains equity in their home, they are more likely to consider purchasing a larger or more attractive home. However, if equity is low, homeowners are likely to remain “equity locked-in” to their home.

Mortgage Rates Expected to Remain Low Through 2021

In the first week of June, many were concerned that the good news from the May jobs report would result in rising mortgage rates. While rates did jump up briefly, they have since fallen back to historic lows. The consensus among real estate and mortgage finance economists is that mortgage rates may fluctuate, but are likely to remain near historic lows through 2021. Our Potential Home Sales Model indicates that even if mortgage rates climbed to 3.5 percent, all else held equal, the market potential for existing-home sales would decrease modestly from 4.92 million SAAR to 4.84 million SAAR. It’s likely that mortgage rates may rise again from their historically low levels, but house-buying power is positioned to remain strong by any reasonable historic standard. Record low mortgage rates are proving to be a powerful motivator and benefit for home buyers in an otherwise challenging time.

May 2020 Potential Home Sales

For the month of May, First American updated its proprietary Potential Home Sales Model to show that:

- Potential existing-home sales increased to a 4.92 million seasonally adjusted annualized rate (SAAR), a 6.2 percent month-over-month increase.

- This represents a 46.5 percent increase from the market potential low point reached in February 1993.

- The market potential for existing-home sales decreased 7.0 percent compared with a year ago, a loss of nearly 368,120 (SAAR) sales.

- Currently, potential existing-home sales is 1.81 million (SAAR), or 26.9 percent below the pre-recession peak of market potential, which occurred in March 2004.

Market Performance Gap

- The market for existing-home sales outperformed its potential by 11.5 percent or an estimated 565,580 (SAAR) sales.

- The market performance gap decreased by an estimated 312,204 (SAAR) sales between April 2020 and May 2020.

First American Deputy Chief Economist Odeta Kushi contributed to this post.

What Insight Does the Potential Home Sales Model Reveal?

When considering the right time to buy or sell a home, an important factor in the decision should be the market’s overall health, which is largely a function of supply and demand. Knowing how close the market is to a healthy level of activity can help consumers determine if it is a good time to buy or sell, and what might happen to the market in the future. That is difficult to assess when looking at the number of homes sold at a particular point in time without understanding the health of the market at that time. Historical context is critically important. Our potential home sales model measures what we believe a healthy market level of home sales should be based on the economic, demographic and housing market environments.

About the Potential Home Sales Model

Potential home sales measures existing-homes sales, which include single-family homes, townhomes, condominiums and co-ops on a seasonally adjusted annualized rate based on the historical relationship between existing-home sales and U.S. population demographic data, homeowner tenure, house-buying power in the U.S. economy, price trends in the U.S. housing market, and conditions in the financial market. When the actual level of existing-home sales are significantly above potential home sales, the pace of turnover is not supported by market fundamentals and there is an increased likelihood of a market correction. Conversely, seasonally adjusted, annualized rates of actual existing-home sales below the level of potential existing-home sales indicate market turnover is underperforming the rate fundamentally supported by the current conditions. Actual seasonally adjusted annualized existing-home sales may exceed or fall short of the potential rate of sales for a variety of reasons, including non-traditional market conditions, policy constraints and market participant behavior. Recent potential home sale estimates are subject to revision to reflect the most up-to-date information available on the economy, housing market and financial conditions. The Potential Home Sales model is published prior to the National Association of Realtors’ Existing-Home Sales report each month.