Since hitting a low point during the initial stages of the pandemic, the only major industry to display immunity to the economic impacts of the coronavirus is the housing market. Housing has experienced a strong V-shaped recovery and is now exceeding pre-pandemic levels. This is largely because the economic distress from the pandemic has created a services-driven recession, disproportionally hurting younger, lower wage renters that are less likely to be homeowners or home buyers.

The bifurcated economic landscape has allowed prospective home buyers who are still employed to channel increased savings towards buying a home, and to take advantage of record low mortgage rates. Weekly purchase applications have surpassed their levels from one year ago for 17 straight weeks, due to a delayed spring season and the heightened demand from low rates. In August, these tailwinds propelled housing market potential to its highest level since 2007, driven by a 5.6 percent month-over-month jump in the market potential for existing-home sales, according to our Potential Home Sales Model.

“Demographic demand and Fed policy keeping rates low has helped housing recover rapidly from the initial stages of the pandemic and remain immune to the ongoing economic impacts of the coronavirus for now, but as with the virus itself, we are not sure if immunity lasts forever.”

Forces Boosting Housing Market Potential to 13-Year High:

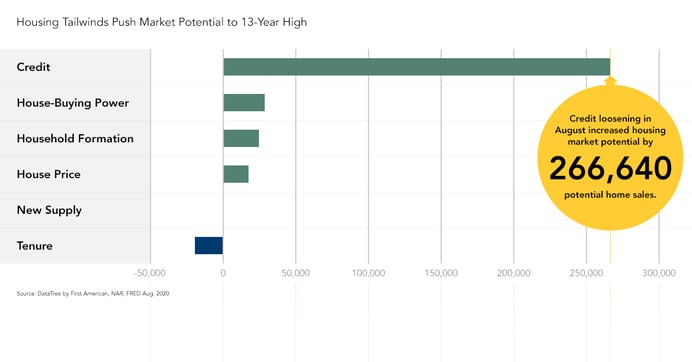

- Credit Loosening: According to the NFCI credit index, a composite measure of credit conditions, credit tightened dramatically in mid-April to its most conservative level since 2009 due to the increased economic uncertainty driven by impacts from the pandemic. Since then, credit availability has loosened, even reaching pre-pandemic levels in August. This credit composite takes into consideration many different credit indicators, giving a comprehensive picture of credit conditions in the U.S. When lending standards are tight, fewer people can qualify for a mortgage to buy a home. Likewise, when standards are loose, more people can qualify for a mortgage and buy a home. Credit loosening in August compared with last month increased housing market potential by 266,640 potential home sales.

- House-Buying Power Increases 1.3%: House-buying power, how much home one can afford to buy given household income and the prevailing mortgage rate, increased 1.3 percent month over month. The house-buying power increase was driven by the combined impact of lower mortgage rates, which were 0.08 percentage points lower in August than the previous month, and a moderate increase in month-over-month household income. The increase in house-buying power boosted market potential by approximately 28,180 potential home sales.

- House Price Appreciation Continues: Homeowners in areas where house prices are rising feel wealthier than those where house prices are flat or declining. As homeowners gain equity in their homes, they are more likely to consider using that equity to purchase a larger or more attractive home – the wealth effect of rising equity. In today’s housing market, fast rising demand against the limited supply of homes for sale has resulted in continued house price appreciation. Compared with last month, the growing wealth effect of rising equity caused by house price appreciation increased housing market potential by nearly 17,270 potential home sales.

- Household Formation Growth Continued: Household formation continued to grow in August, as millennials continued to form new households, increasing demand for housing. Rising household formation increased market potential by 24,255 potential home sales in August compared with last month.

Forces Reducing Housing Market Potential:

- Tenure Length Continues to Rise: Tenure length, the average length of time someone lives in their home, increased 0.5 percent in August relative to last month. The increase in tenure length had a negative impact on housing market potential, reducing it by 20,070 potential home sales compared with last month. While low mortgage rates can spur homebuying demand by reducing the monthly cost of a mortgage and increasing house-buying power, many existing owners who have refinanced into lower mortgages are less incented to move. Since roughly two-thirds of all home buyers are existing homeowners, homeowners staying put reduces the available inventory of homes for sale for home buyers

Is the Pace of Growth Sustainable?

Our Potential Home Sales Model measures what we believe a healthy level of home sales should be based on the economic, demographic and housing market conditions. The market potential for home sales increased to a 13-year high this month due to strong underlying fundamentals, especially the return to pre-pandemic credit conditions. Demographic demand and Fed policy keeping rates low has helped housing recover rapidly from the initial stages of the pandemic and remain immune to the ongoing economic impacts of the coronavirus for now, but as with the virus itself, we are not sure if immunity lasts forever.

August 2020 Potential Home Sales

For the month of August, First American updated its proprietary Potential Home Sales Model to show that:

- Potential existing-home sales increased to a 5.92 million seasonally adjusted annualized rate (SAAR), a 5.6 percent month-over-month increase.

- This represents a 70.8 percent increase from the market potential low point reached in February 1993.

- The market potential for existing-home sales increased 9.7 percent compared with a year ago, a gain of nearly 525,580 (SAAR) sales.

- Currently, potential existing-home sales is 875,000 million (SAAR), or 12.9 percent below the pre-recession peak of market potential, which occurred in April 2006.

Market Performance Gap

- The market for existing-home sales underperformed its potential by 4.8 percent or an estimated 282,430 (SAAR) sales.

- The market performance gap increased by an estimated 271,060 (SAAR) sales between July 2020 and August 2020.

First American Deputy Chief Economist Odeta Kushi contributed to this post.

What Insight Does the Potential Home Sales Model Reveal?

When considering the right time to buy or sell a home, an important factor in the decision should be the market’s overall health, which is largely a function of supply and demand. Knowing how close the market is to a healthy level of activity can help consumers determine if it is a good time to buy or sell, and what might happen to the market in the future. That is difficult to assess when looking at the number of homes sold at a particular point in time without understanding the health of the market at that time. Historical context is critically important. Our potential home sales model measures what we believe a healthy market level of home sales should be based on the economic, demographic and housing market environments.

About the Potential Home Sales Model

Potential home sales measures existing-home sales, which include single-family homes, townhomes, condominiums and co-ops on a seasonally adjusted annualized rate based on the historical relationship between existing-home sales and U.S. population demographic data, homeowner tenure, house-buying power in the U.S. economy, price trends in the U.S. housing market, and conditions in the financial market. When the actual level of existing-home sales are significantly above potential home sales, the pace of turnover is not supported by market fundamentals and there is an increased likelihood of a market correction. Conversely, seasonally adjusted, annualized rates of actual existing-home sales below the level of potential existing-home sales indicate market turnover is underperforming the rate fundamentally supported by the current conditions. Actual seasonally adjusted annualized existing-home sales may exceed or fall short of the potential rate of sales for a variety of reasons, including non-traditional market conditions, policy constraints and market participant behavior. Recent potential home sale estimates are subject to revision to reflect the most up-to-date information available on the economy, housing market and financial conditions. The Potential Home Sales model is published prior to the National Association of Realtors’ Existing-Home Sales report each month.