The housing market has faced its fair share of headwinds leading up to this year’s spring home-buying season. While mortgage rates have retreated from recent highs, they remain elevated compared with one year ago, and house prices, while down from the peak, also remain elevated. All while housing supply remains historically and unseasonably low. These headwinds are not new to the housing market, but there is a new concern on the horizon – tightening credit standards.

“While credit conditions tightened slightly in the March NFCI report, it’s unlikely that the recent banking crisis will materially impact residential mortgage availability.”

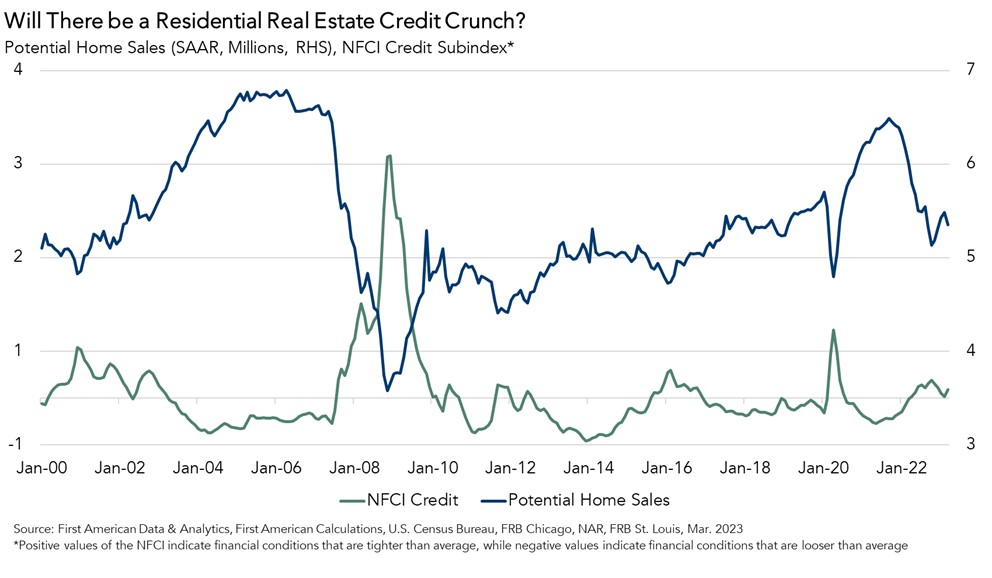

Our Potential Home Sales Model, which measures what we believe a healthy market for home sales should be, based on the economic, demographic and housing market environments, dipped this month, and the biggest reason for the month-over-month loss was tightening credit conditions. At the onset of the pandemic, tighter credit was the biggest contributor to the loss of potential home sales, as lenders reduced credit to account for a higher likelihood of forbearance and delinquency. The Potential Home Sales Model uses the Chicago Fed National Financial Conditions Credit Subindex (NFCI), which is a comprehensive indicator of credit conditions. Given the recent banking crisis, let’s examine how and why credit conditions may affect the housing market.

This Time it’s Different

There are fears that the recent bank failures will prompt lenders to be much more conservative with their lending. At a high level, when lending standards are tight, fewer people can qualify for a mortgage to buy a home. When homeowners are less likely to qualify for a mortgage, they are more likely to stay in their current home or, for potential first-time home buyers, not buy one at all. Credit tightening can come in many forms. For example, the availability of mortgages or other loan products may fall, or it may become more difficult to qualify for a mortgage because of lender requirements for higher credit scores, lower debt-to-income ratios, or larger down payments or greater cash reserves.

While the NFCI Credit index indicated that credit tightened in March, which reduced housing market potential, the credit tightening was modest and far from recent pandemic lows, and certainly nothing like the Great Financial Crisis (GFC) period. One of the reasons that the residential mortgage sector may be protected from credit tightening is that mortgage lending is less sensitive to bank balance sheet pressures.

According to a recent analysis from Goldman Sachs, only 18 percent of mortgages are held on bank balance sheets, while nearly 70 percent of outstanding mortgages are securitized into mortgage-backed securities, so the lender doesn’t have to fund the loan from their deposits or manage the credit risk. The securitization market, dominated by government agencies (Fannie Mae, Freddie Mac and Federal Housing Administration), sets the mortgage eligibility requirements.

Mortgages typically held on bank balance sheets include non-conforming and jumbo loans. Lenders may tighten lending requirements for these balance-sheet products. In fact, in a recent report, the Mortgage Bankers Association indicated that mortgage rates for jumbo loans increased, while rates for conforming loans declined. The divergence in rates suggests that banks may be tightening credit in response to banking uncertainty for those products. By tightening credit and limiting the number of jumbo loans they originate, banks can reduce their exposure to credit risk and conserve their cash if needed.

Affordability and lack of inventory remain the primary challenges to housing market potential. While credit conditions tightened in the March NFCI report, it’s unlikely that the recent banking crisis will materially impact residential mortgage availability. Additionally, the GFC and pandemic fears of foreclosure and forbearance are not top of mind for lenders.

March 2023 Potential Home Sales

For the month of March, First American updated its proprietary Potential Home Sales Model to show that:

- Potential existing-home sales decreased to a 5.35 million seasonally adjusted annualized rate (SAAR), a 2.5 percent month-over-month decrease.

- This represents a 53.5 percent increase from the market potential low point reached in February 1993.

- The market potential for existing-home sales decreased 10.7 percent compared with a year ago, a loss of 641,700 (SAAR) sales.

- Currently, potential existing-home sales is 1,439,400 (SAAR), or 21.2 percent below the pre-recession peak of market potential, which occurred in April 2006.

First American Deputy Chief Economist Odeta Kushi contributed to this post.

What Insight Does the Potential Home Sales Model Reveal?

When considering the right time to buy or sell a home, an important factor in the decision should be the market’s overall health, which is largely a function of supply and demand. Knowing how close the market is to a healthy level of activity can help consumers determine if it is a good time to buy or sell, and what might happen to the market in the future. That is difficult to assess when looking at the number of homes sold at a particular point in time without understanding the health of the market at that time. Historical context is critically important. Our potential home sales model measures what we believe a healthy market level of home sales should be based on the economic, demographic and housing market environments.

About the Potential Home Sales Model

Potential home sales measures existing-home sales, which include single-family homes, townhomes, condominiums and co-ops on a seasonally adjusted annualized rate based on the historical relationship between existing-home sales and U.S. population demographic data, homeowner tenure, house-buying power in the U.S. economy, price trends in the U.S. housing market, and conditions in the financial market. When the actual level of existing-home sales are significantly above potential home sales, the pace of turnover is not supported by market fundamentals and there is an increased likelihood of a market correction. Conversely, seasonally adjusted, annualized rates of actual existing-home sales below the level of potential existing-home sales indicate market turnover is underperforming the rate fundamentally supported by the current conditions. Actual seasonally adjusted annualized existing-home sales may exceed or fall short of the potential rate of sales for a variety of reasons, including non-traditional market conditions, policy constraints and market participant behavior. Recent potential home sale estimates are subject to revision to reflect the most up-to-date information available on the economy, housing market and financial conditions. The Potential Home Sales model is published prior to the National Association of Realtors’ Existing-Home Sales report each month.