It’s been a long time coming – a rising rate environment. The 30-year, fixed-rate mortgage has been below 4.5 percent since late 2013 and is now finally moving consistently higher. According to the consensus of economic forecasts, it is likely to approach 5 percent by the end of this year. This matters for defect, fraud and misrepresentation risk as rising mortgage rates reduce the benefit of refinancing and increase the share of purchase loan transactions in the market. As we have noted before, purchase loan transactions are riskier than refinance transactions.

“Today’s ARM is not like those of the past. It is essentially the same as the 30-year, fixed-rate mortgage with one difference – rates adjust after an initial fixed period of usually five or seven years.”

But, there is another reason why a rising rate environment matters for defect, fraud and misrepresentation risk. The allure of the adjustable-rate mortgage (ARM) increases. The current rate on a 30-year, fixed-rate mortgage is approximately 4.5 percent. Yet, there is another mortgage option – the ARM, which typically has a lower rate than the traditional 30-year, fixed-rate mortgage. Currently, ARMs are available at about 4 percent. As rates increase and borrowers seek to keep their monthly payment low, more borrowers are likely to choose the adjustable-rate option.

A Kinder, Gentler, Less Risky ARM

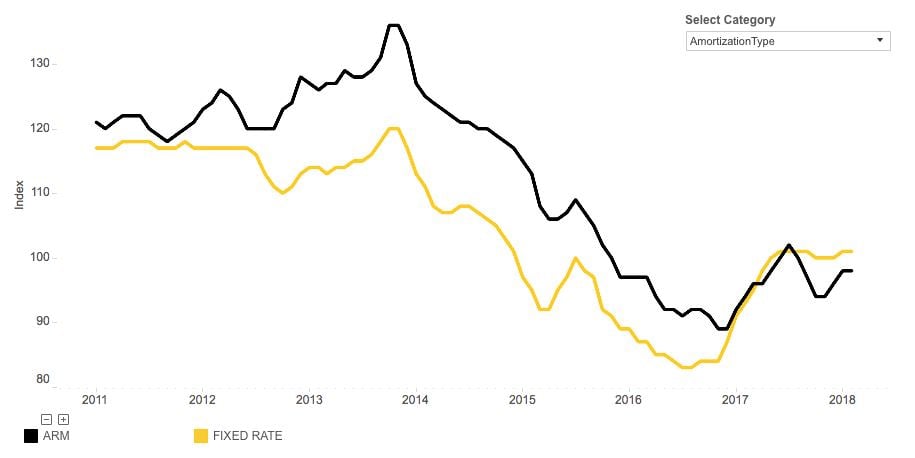

ARMs historically have had more defect, fraud and misrepresentation risk than the traditional 30-year, fixed rate mortgage. Interestingly, that has changed recently. Adjustable-rate mortgages, based on our defect, fraud and misrepresentation index, are modestly less risky.

At the height of the housing boom, adjustable-rate mortgages were all the rage, and many included additional elements that added risk, such as negative amortization, payment-option and interest-only options, and teaser rate ARMs. Today’s ARM is not like those of the past. It is essentially the same as the 30-year, fixed-rate mortgage with one difference – rates adjust after an initial fixed period of usually five or seven years. Saving half a percent on the mortgage rate may be worthwhile for many consumers, especially if their expected tenure length in the house is not 30 years.

As mortgage rates continue to rise, the share of adjustable-rate mortgages is also likely to increase and, if current defect risk patterns hold, will offset some of the increased risk the market will bear as it shifts to purchase transactions.

For the top five states and markets where defect risk is increasing or decreasing, and more, please visit the Loan Application Defect Index.