The market potential for existing-home sales in May fell 2 percent to 5.62 million at a seasonally adjusted annualized rate (SAAR), compared with last month, and is 10.5 percent lower than one year ago. Yet, the market potential for home sales remains 2.5 percent higher than May 2019, before the pandemic hit.

“You can’t buy what’s not for sale -- and existing homeowners have little incentive to relieve the supply pressure, keeping a lid on housing market normalization.”

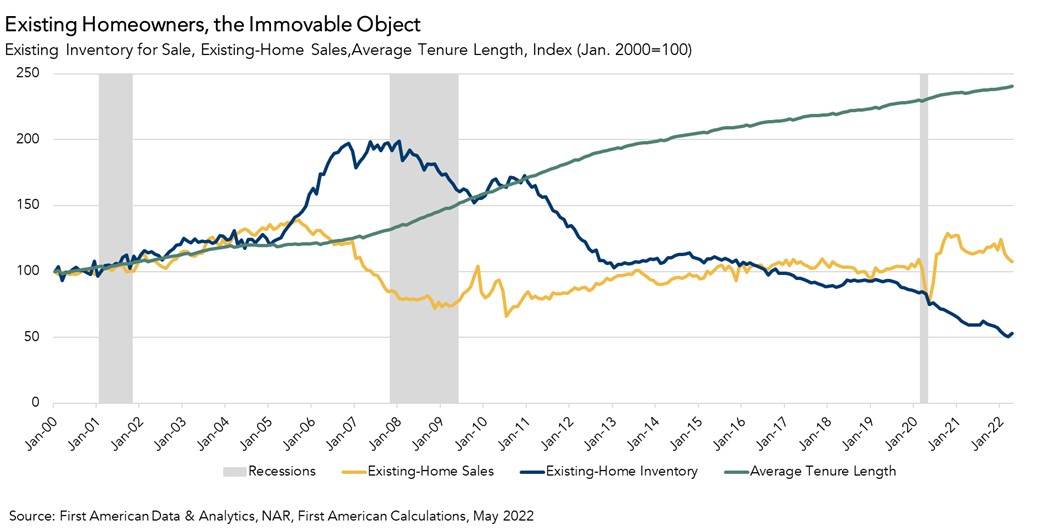

Home purchase demand is declining as mortgage rates rise alongside still-strong house price appreciation. While a decline in demand may reduce the pace of sales and lead to an increase in inventory, existing homeowners are less inclined to sell their homes as mortgage rates rise. Historically, nearly 90 percent of total inventory is existing-home inventory, and existing homeowners are staying put. Increasing the supply of homes for sale is key to slowing house price growth and restoring balance to the housing market.

Existing Homeowners, the Immovable Object

The amount of time a typical homeowner lives in their home increased 2 percent from one year ago, and 0.4 percent compared with last month, which was the largest month-over-month increase since August 2020 and contributed to a loss of 15,500 potential home sales compared with last month. Since existing homeowners supply the majority of the homes for sale, and homeowners are staying put longer, the housing market faces an ongoing supply shortage.

Before the housing market crash in 2007, the average length of time someone lived in their home was approximately five years. During the aftermath of the housing market crisis between 2008 and 2016, the average length of time someone lived in their home grew to approximately eight years. The most recent data shows that the average length of time someone lives in their home reached a historic high of 10.6 years in May 2022.

Two Trends Limiting Housing Supply and Housing Market Normalization

Two trends are locking homeowners in place, preventing much-needed housing supply from reaching the market and helping tilt the market toward buyers. Many existing homeowners are rate locked-in to historically low, sub-3 percent mortgage rates, and now that rates are rising, there is a financial disincentive to sell their homes and buy a new home at a higher mortgage rate. The golden handcuffs of low mortgage rates prevent more supply from reaching the market.

Seniors choosing to age in place, rather than downsize or move to another home, further limits housing supply. A 2019 study from Freddie Mac shows that if adults born between 1931-1959 behaved like earlier generations, they would have released nearly 1.6 million additional housing units to the market by 2018. As seniors continue to choose to age in place, there will be fewer existing homes available for sale. And, with many of these senior homeowners also locked into historically low mortgage rates and sitting on historically high levels of equity, it’s more likely they will renovate the home they currently own than list their home for sale and move.

What Does it all Mean for the Housing Market?

A moderation of house price growth will signal that balance is returning to the housing market. Yet, more housing supply is critical to meaningful moderation in house price appreciation. While rising mortgage rates will continue to cool demand, it will also keep existing homeowners locked into their homes. You can’t buy what’s not for sale -- and existing homeowners have little incentive to relieve the supply pressure, keeping a lid on housing market normalization.

May 2022 Potential Home Sales

For the month of May, First American updated its proprietary Potential Home Sales Model to show that:

- Potential existing-home sales decreased to a 5.62 million seasonally adjusted annualized rate (SAAR), a 2.0 percent month-over-month decrease.

- This represents a 61.2 percent increase from the market potential low point reached in February 1993.

- The market potential for existing-home sales decreased 10.5 percent compared with a year ago, a loss of 660,395 (SAAR) sales.

- Currently, potential existing-home sales is 1,171,000 (SAAR), or 17.2 percent below the pre-recession peak of market potential, which occurred in April 2006.

First American Deputy Chief Economist Odeta Kushi contributed to this post.

What Insight Does the Potential Home Sales Model Reveal?

When considering the right time to buy or sell a home, an important factor in the decision should be the market’s overall health, which is largely a function of supply and demand. Knowing how close the market is to a healthy level of activity can help consumers determine if it is a good time to buy or sell, and what might happen to the market in the future. That is difficult to assess when looking at the number of homes sold at a particular point in time without understanding the health of the market at that time. Historical context is critically important. Our potential home sales model measures what we believe a healthy market level of home sales should be based on the economic, demographic and housing market environments.

About the Potential Home Sales Model

Potential home sales measures existing-home sales, which include single-family homes, townhomes, condominiums and co-ops on a seasonally adjusted annualized rate based on the historical relationship between existing-home sales and U.S. population demographic data, homeowner tenure, house-buying power in the U.S. economy, price trends in the U.S. housing market, and conditions in the financial market. When the actual level of existing-home sales are significantly above potential home sales, the pace of turnover is not supported by market fundamentals and there is an increased likelihood of a market correction. Conversely, seasonally adjusted, annualized rates of actual existing-home sales below the level of potential existing-home sales indicate market turnover is underperforming the rate fundamentally supported by the current conditions. Actual seasonally adjusted annualized existing-home sales may exceed or fall short of the potential rate of sales for a variety of reasons, including non-traditional market conditions, policy constraints and market participant behavior. Recent potential home sale estimates are subject to revision to reflect the most up-to-date information available on the economy, housing market and financial conditions. The Potential Home Sales model is published prior to the National Association of Realtors’ Existing-Home Sales report each month.