By now, everyone in the mortgage industry is aware that we are entering a market that will be dominated by purchase demand for the next several years. According to the latest Mortgage Bankers Association forecast, refinance transactions will make up 28 percent of total mortgages originated in 2018 and is forecasted to drop to 23 percent by 2020. This is, of course, due to the current environment of increasing mortgage rates that follows years of persistently low rates. Until last month, the average rate for a 30-year fixed mortgage had remained below 4.5 percent for 80 consecutive months. And since most homeowners have benefited from the low-rate environment, they now have little financial incentive to refinance, or sell and buy again. With mortgage rates continuing to rise, the financial value of keeping their current low-rate mortgages is likely to increase.

“It’s likely that all of the investment in more digitized, automated, and efficient mortgage manufacturing and underwriting technology that’s been made in recent years is beginning to pay off,” says Chief Economist Mark Fleming.

The silver lining? Despite the aforementioned obstacles, consumers will continue to buy. Richard Thaler, Nobel Prize-winning economist, is famous for the analogy that we are more like Homer Simpson than Spock when making economic decisions. Lifestyle decisions will still incentivize people to buy, and sometimes that beautiful kitchen is just too hard to resist! Again, according to the Mortgage Bankers Association forecast, the purchase market is expected to grow even as mortgage rates rise, largely on the strength of first-time homebuyer demand.

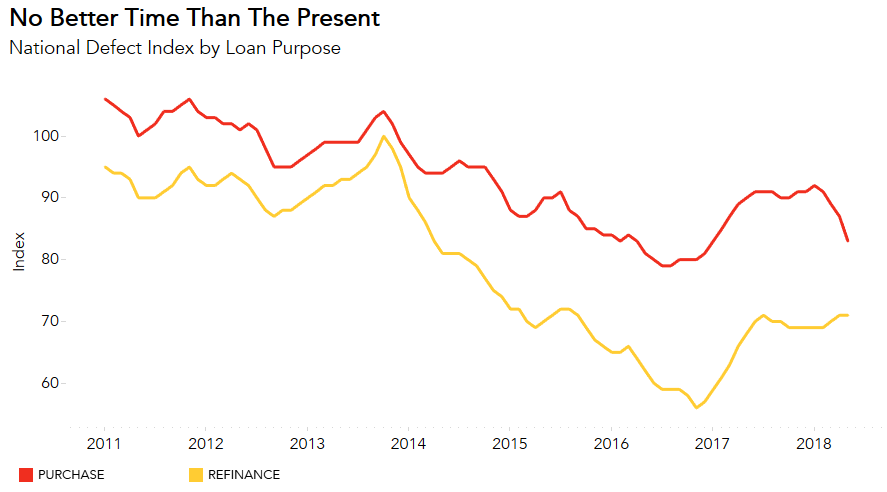

With this fact in mind, the most important news in this month’s Loan Application Defect Index (LADI) is that the Defect Index for purchase transactions decreased by 4.6 percent compared with the previous month, is down 7.8 percent compared with a year ago, and has declined almost 10 percent in just the past five months. There’s no better time to have loan application misrepresentation, defect and fraud risk on purchase transactions on the decline than when the market share of purchase transactions is rising.

It’s likely that all of the investment in more digitized, automated, and efficient mortgage manufacturing and underwriting technology that’s been made in recent years is beginning to pay off. Now the question is, how much lower will it go?

For Mark’s full analysis on loan defect risk, the top five states and markets with the greatest increases and decreases in defect risk, and more, please visit the Loan Application Defect Index.

The Defect Index is updated monthly with new data. Look for the next edition of the Defect Index the week of July 29, 2018.