This Valentine’s Day, while couples nationwide enjoy romantic dinners, exchange chocolates and flowers, or cozy up at home with a nicer-than-average bottle of wine, economists will instead be focusing on something slightly less romantic: how much money people are spending on retail goods and services.

While the retail sales report that comes out the day after Valentine’s Day will not yet reflect February spending, many will still be focused on it. The latest retail sales report from December showed that consumers were still spending a lot of money. However, with the job market softening, and the probability of a recession still uncertain, the strength of the American consumer remains front of mind, especially since consumer spending makes up 70 percent of economic growth. For commercial real estate (CRE) professionals, the strength of the U.S. consumer and the economy is an important determinant of everything from demand for CRE to the investment and lending climate. As such, today’s X-Factor will take a closer look at one of the greatest determinants of economic growth: the surprising strength of consumer spending and whether or not consumers can keep it up.

“In the meantime, continued strong consumer spending will buoy the economy, increase GDP growth, and decrease the chance of a recession, making it more difficult for the Federal Reserve to justify interest rate cuts sooner.”

When Does a Trend Become a Trend?

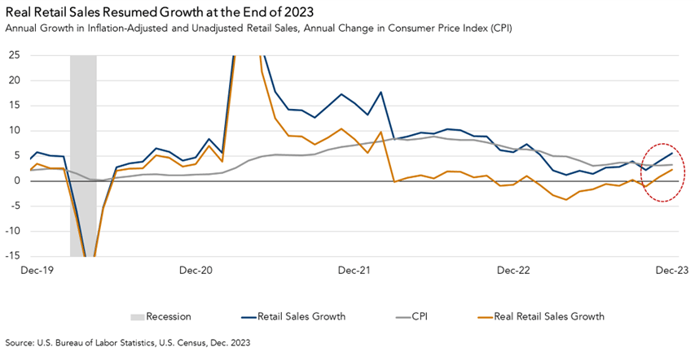

Real retail sales is an inflation-adjusted measure that represents a change in spending activity without the noise of economy-wide price increases. The chart below shows that real retail sales growth was negative for most of 2023. Only towards the end of the year did retail sales begin to grow in real terms. In November, real retail sales grew at 0.8 percent, and in December at 2.3 percent. While one or even two months of positive growth may not constitute a trend, a third month likely does. If the post-Valentine’s Day retail sales report shows another gain in real terms, it will be an indication that the American consumer remains resilient.

Non-Experiential Real Retail Sales Jumped in December 2023

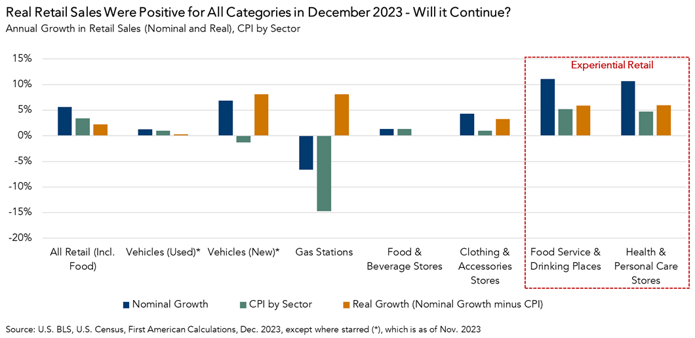

Another twist in the December 2023 retail data was not just that headline real retail sales grew, but that spending in categories that had been in decline for most of 2023 also increased. Throughout most of 2023, non-experiential retail categories, like apparel or food and beverage stores declined, whereas experiential categories, like restaurants and salons continued to grow. In December, however, no major categories declined in real terms. That means that in the 2023 holiday season people bought more goods in real terms than they did during the 2022 holiday season, while also continuing to dine out.

The Savings Cushion Remains

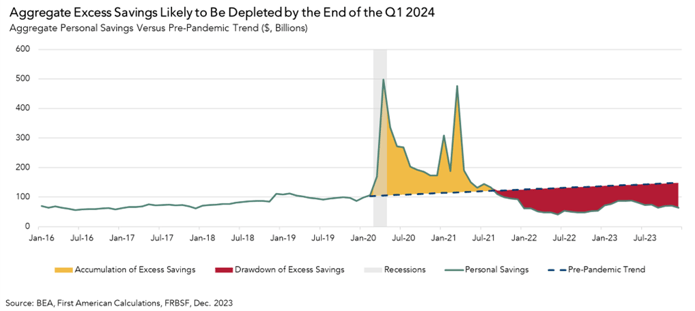

So, what’s driving this spending? Excess pandemic-era savings is part of the story. When the pandemic hit in 2020, the savings rate skyrocketed, and consumers accumulated a stock of excess savings. Since mid-2021, those excess funds have been spent down and are nearing depletion. The latest estimate from the Federal Reserve of remaining excess savings is about $430 billion. With an estimated depletion rate of about $75 billion per month, the outstanding stock of excess savings should be entirely depleted sometime in the second quarter of this year.

The Consumer is Borrowing More, but Less than Headlines Suggest

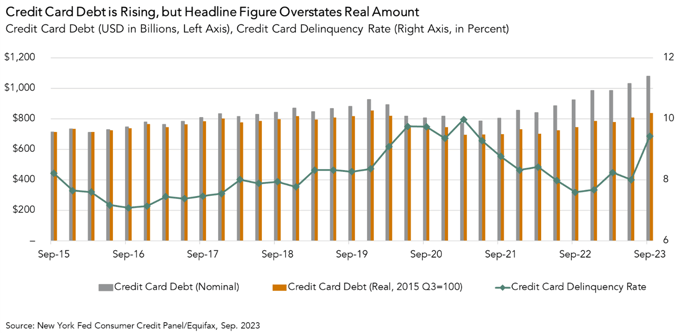

On a recent episode of The REconomy Podcast™, our economics team answered a listener’s question about rising credit card debt. In answering that question, it was highlighted that, while the quantity of credit card debt is at an all-time high, it is not an inflation-adjusted figure. This makes the “credit card debt is at all-time highs” statement a little less meaningful, as comparing across time periods is not apples-to-apples when the data isn’t inflation adjusted.

In real terms, credit card debt is rising, but at a slower pace. Credit card debt in real terms has increased, but remains below its all-time peak, which occurred in the fourth quarter of 2019, right before the pandemic struck. Consumers paid down a lot of credit card debt through 2020 and into 2021, but since mid-2022 have been borrowing more. With interest rates higher, that means more money spent on interest expense and less on retail goods and services.

Fed May Not Have Urgency to Cut Rates Until Second Half of 2024

We won’t know how consumers will have spent money this Valentine’s Day until the March retail sales release. But, with the post-Valentine’s Day retail sales report, we will have a third data point that may confirm an upward trend in real retail sales growth. That would signal that American consumers are continuing to spend, despite headwinds from higher interest rates on larger amounts of credit card debt and the resumption of student loan payments.

Given this combination and the ongoing depletion of excess pandemic savings, it seems likely that real retail sales growth will slow in the second half of this year. In the meantime, continued strong consumer spending will buoy the economy and decrease the chance of a recession, making it more difficult for the Federal Reserve to justify interest rate cuts sooner.