The millennial generation, those born between 1981 and 1996, have recently dominated the demand side of the housing market. However, Generation Z, those born between 1997 and 2012, is on the cusp of aging into their prime home-buying years. While potential first-time home buyers, mostly millennials and older Gen Zers, jumped on the historically low mortgage rates available in 2020 and 2021, those looking to shift from renting to homeownership in 2023 face mortgage rates that are nearly 4 percentage points higher than the low point in the fourth quarter of 2020, limiting their purchasing power. As potential first-time home buyers consider homeownership, they should carefully weigh the costs of renting against the costs of owning a home, which varies greatly by market.

One year ago in the second quarter of 2022, it was cheaper to own a home than to rent nationally and in all 50 of the top U.S. markets thanks to near-record low mortgage rates and rapid house price appreciation. A year later, substantial increases in mortgage rates, coupled with declining house prices in some markets, tipped the scales in the opposite direction. In the second quarter of 2023, it was cheaper to rent than to own nationally and in 27 of the top 50 U.S. markets.

“Once you factor in house price appreciation, or depreciation in some markets, to the cost of homeownership, the decision to rent or buy will depend on local real estate market dynamics, which will determine if a home is likely to cost more or less in the near future.”

The Affordability Shift from Homeownership to Renting

What goes into the monthly cost of renting or owning? The cost of renting is simply the amount of rent paid every month. The monthly cost of owning a home includes taxes, repairs, homeowner’s insurance and the monthly mortgage principal and interest payments. To calculate the monthly cost of homeownership, our analysis assumes the hypothetical first-time home buyer is taking out a 30-year, fixed-rate mortgage with a 5 percent down payment on a home at the 25th percentile sale price in their market in the second quarter of 2023. Finally, the monthly cost to own factors in the potential benefit of equity accumulation through house price appreciation.

Rising house prices increase the cost to buy, all else held equal, for the potential home buyer. However, rising home prices provide the homeowner with the benefit of equity accumulation. On the other hand, declining house price appreciation results in a loss of equity and, therefore, is considered a cost for the homeowner.

Nationally, house price appreciation was 2 percent year over year in the second quarter of 2023, according to our First American Data & Analytics house price index. However, house price appreciation was not uniform across markets, with house prices declining up to 9 percent in some markets, while increasing as much as 14 percent in others. As a result, the difference in the monthly cost of renting and owning varied significantly from market to market.

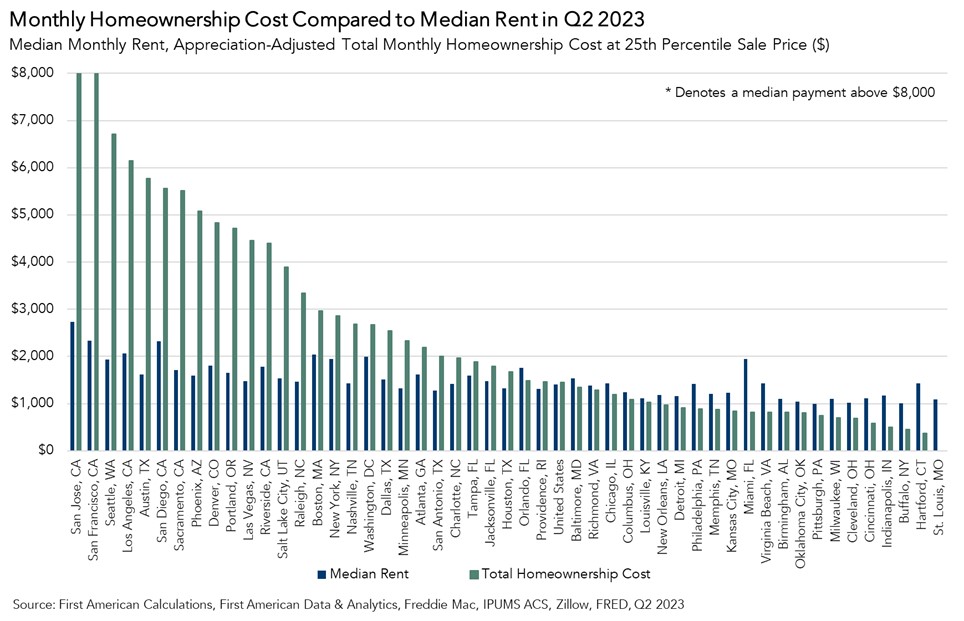

Diverging Affordability

In many large markets, the monthly cost of homeownership far outpaced the cost of rent in the second quarter of 2023. In Seattle, for example, the median rent was approximately $1,930 and the homeownership cost was $6,720. Along with the upfront costs of homeownership, house price appreciation plays a critical role in the financial decision to rent or own.

Last year, house price appreciation was positive across the top 50 U.S. markets, but in the second quarter of 2023, house prices declined in 15 markets, adding to the monthly ownership costs in those markets. In Seattle, house price depreciation added approximately $2,500 to the monthly cost of ownership. While this cost is not an explicit part of the homeowner’s mortgage payment every month, the decline in equity still informs a potential first-time home buyer’s behavior. Why buy a home now, when you may be able to buy it for less in the future?

Conversely, in many Midwestern and Southern cities, such as Birmingham, Ala. and Cleveland, it was cheaper to own than rent. In Cleveland, the monthly cost of rent in the second quarter of 2023 was $1,020, while the monthly cost of homeownership was approximately $1,740, before accounting for house price appreciation. Annual house price appreciation in Cleveland was 4.4 percent in the second quarter of 2023, making the equity-adjusted monthly homeownership cost $690, $330 less than the monthly cost of renting. As younger generations consider their housing options, the greater opportunity to transition to homeownership in these more affordable markets may become more attractive to potential first-time home buyers. In other words, buy the home now because it will likely cost you more to buy it in the future.

What’s the Outlook for Generation Z?

Given current dynamics, more young households may choose to rent in the near term as the cost to own, excluding house price appreciation, has unequivocally increased. Yet, once you factor in house price appreciation, or depreciation in some markets, to the cost of homeownership, the decision to rent or buy will depend on local real estate market dynamics, which will determine if a home is likely to cost more or less in the near future.

Methodology

The rent-versus-buy analysis compares monthly rental payments with the cost of ownership in the top 50 U.S. metropolitan cities. Median rent is calculated from the 2021 American Community Survey micro data, the latest year available, and extrapolated to Q2 2023 using the Zillow Observed Rent Index. Home price sales, property tax rates, and house price appreciation by market are derived from First American Data & Analytics data. Further, the monthly ownership cost is calculated by combining monthly mortgage payments, interest, taxes and insurance (PITI), assuming a down payment of 5 percent and an interest rate of 6.5 percent, which is the average for a 30-year, fixed rate mortgage in Q2 2023. Because the down payment assumed is less than 20 percent, private mortgage insurance is added to the cost of ownership at a rate of 0.75 percent of the home value. Annual homeowner’s insurance is assumed to be 0.4 percent of the home value, and annual repair costs are assumed to be 1 percent of the home value.

Juliette Barragan contributed to this blog post.

.jpg)