Last week, the average 30-year, fixed-rate mortgage rose 5 basis points to 4.46 percent, reaching its highest level since January of 2014. The consensus among economists is that the 30-year, fixed-rate mortgage will approach 5 percent by the end of this year. All else held equal, this will make housing more expensive. However, some perspective is important. The historical average for the 30-year, fixed-rate mortgage is about 8 percent so, even with the expected increase, mortgage rates will still be low by historical standards.

"The supply squeeze and rising mortgage rates are powerful forces working against housing affordability, but homeowners are gaining equity and the economy remains strong."

The primary reason mortgage rates are rising is a healthy and growing economy. Income levels are growing in many markets, which helps offset rising interest rates. Nationally, house-buying power, how much one can buy based on changes in income and interest rates, has increased by 0.8 percent in the past year. However, some markets have seen faster income growth and subsequently greater increases in house-buying power – Riverside, Calif. (+4.5 percent), San Francisco (+3.5 percent), and Providence, Rhode Island (+2.8 percent) led the nation.

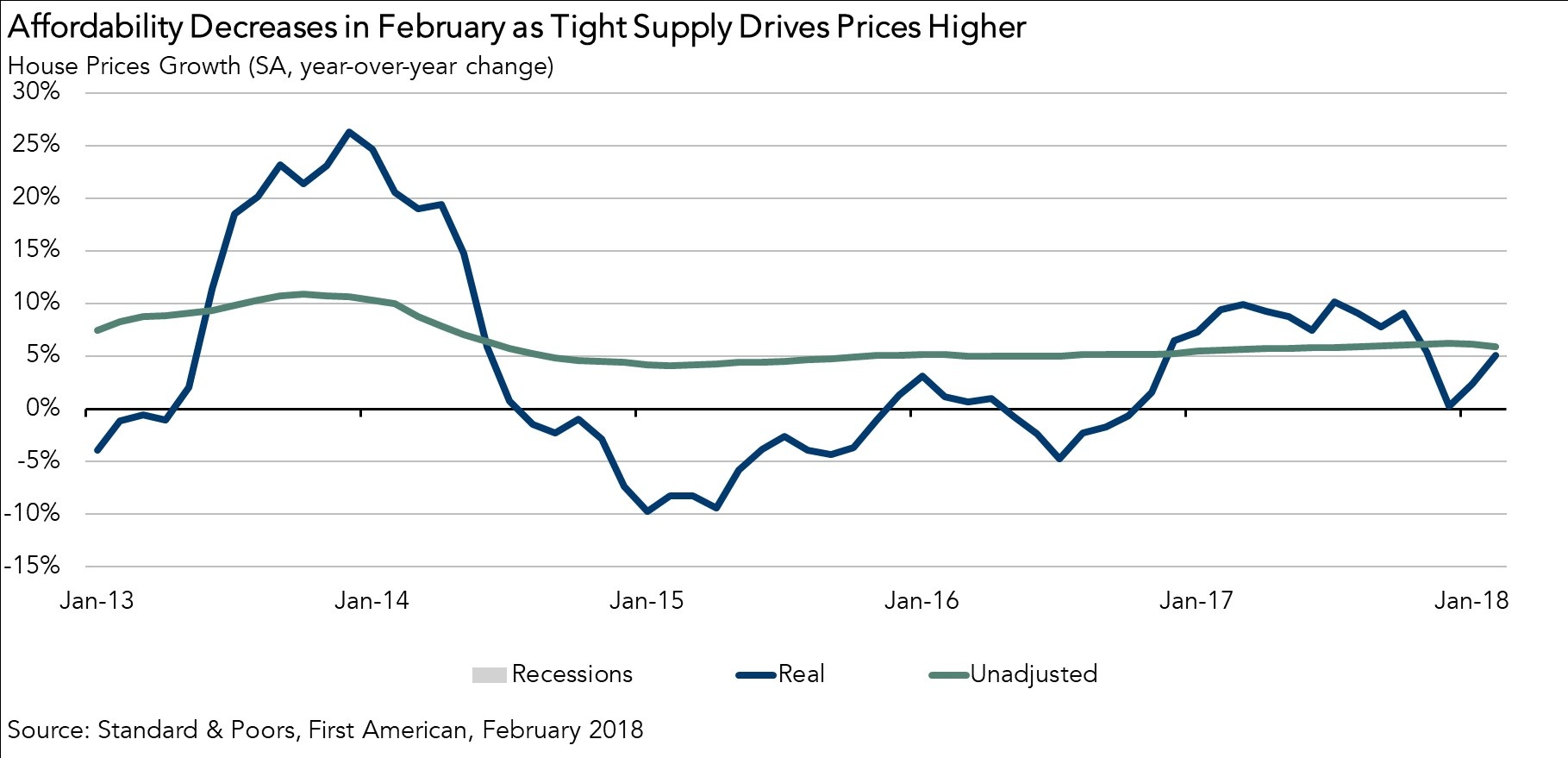

So, if house-buying power has increased, meaning consumers can afford to purchase more home, why is affordability declining as illustrated by increases in our Real House Price Index of 2.9 percent month over month and over 5 percent since last year? Two words: supply squeeze.

The Supply Squeeze is On

Two dynamics are restricting housing supply this spring, namely an increasing number of homeowners are rate-locked, and the prisoner’s dilemma facing homeowners. The supply squeeze is already impacting the market. Existing-home sales, which account for roughly 90 percent of U.S. home sales, declined 1.3 percent in February compared with a year ago. The market is underperforming its potential by an estimated 300,000 seasonally adjusted annualized rate of sales. The risk of selling one’s home in a market with a shortage of inventory keeps existing homeowners from selling, preventing more supply from entering the market. This increases competition for homes and puts pressure on prices. Not surprisingly, unadjusted house prices increased 5.9 percent in February compared with a year ago.

Relief on the Horizon?

The supply squeeze and rising mortgage rates are powerful forces working against housing affordability, but homeowners are gaining equity and the economy remains strong. Millennial demand for homeownership is growing and builders remain confident, demonstrated by the number of homes under construction reaching its highest point in more than a decade in February. The conditions driving the supply squeeze, upward pressure on prices and consequently lower affordability are likely to continue through 2018. However, some relief may be on the horizon, as more homes are on the way and income gains are offsetting rising interest rates. That’s good for the housing market.

For Mark’s full analysis on affordability, the top five states and markets with the greatest increases and decreases in real house prices, and more, please visit the Real House Price Index.

The RHPI is updated monthly with new data. Look for the next edition of the RHPI the week of May 21, 2018.