While there is a substantial quantity of commercial real estate (CRE) debt maturing this year, there’s nothing inherently dangerous about a mortgage coming due. Challenges arise when maturities occur simultaneously with one of two other challenges. The first is when a building is not generating sufficient income to cover its expenses, which is sometimes referred to as a “liquidity” issue. The second is when a building’s value falls below the outstanding balance of its mortgage, which is an example of a “solvency” issue. When a commercial property is insolvent, it is said to be “underwater.”

Though both illiquidity and insolvency are types of CRE distress, they are distinct situations with different implications for property owners and operators. When both illiquidity and insolvency are present, the risk of distress is highest. In this scenario, the building can’t pay its bills and the equity in the building is not enough to cover the balance of the loan in a sale. This is the “dual trigger” of foreclosure.

“Illiquidity and insolvency present different challenges for operators. Each ‘trigger’ is necessary, but insufficient on its own to force foreclosure and it’s worth bearing this distinction in mind.”

Illiquidity and Insolvency: Today’s Problem Vs. Tomorrow’s

Of these two types of distress, lack of liquidity is arguably the most pressing as it means a building’s income from operations isn’t meeting its immediate expenses. If nothing is done to rectify the situation, then the owner could run out of cash, at least within that building’s operating entity. Lack of liquidity means a clock is ticking and something must be done before time runs out.

Insolvency issues also have a time limit to rectify, but often a longer one than liquidity issues. If an insolvent building is still generating enough income to pay its daily expenses, including debt payments, its owner can hold and wait until prices recover and the value of their property comes back “above water.” In other words, a commercial property with an underwater mortgage can still be liquid. As long as a building’s cash flow is meeting its operating expenses, time is at least somewhat on the building owner’s side.

Unlike residential loans, CRE loans do not always require principal repayments throughout the life of the mortgage, or if they do, they may only require a portion of principal to be paid. As a result, there is usually a larger remaining balance of debt outstanding, referred to as a “balloon payment” at the loan’s maturity date. Insolvency becomes an immediate problem when a building’s mortgage matures, and the owner needs to refinance, but is unable to find a replacement mortgage that’s large enough to pay off the remaining balance of their current one.

How is the Industry Measuring Up?

Today, not all asset classes are performing the same. Office properties specifically are struggling with both liquidity and insolvency challenges. One measure of liquidity is a debt service coverage ratio (“DSCR”), which compares how much income a property makes relative to the size of its mortgage payment. A DSCR greater than 1 indicates that a building is generating enough profit to fully pay its mortgage, while a DSCR less than 1 indicates that income is insufficient to meet the building’s mortgage payments. According to data from Trepp, approximately 11 percent of all outstanding office Collateralized Mortgage-Backed Securities (CMBS, a type of CRE loan) have a DSCR under 1, the highest of any asset class.

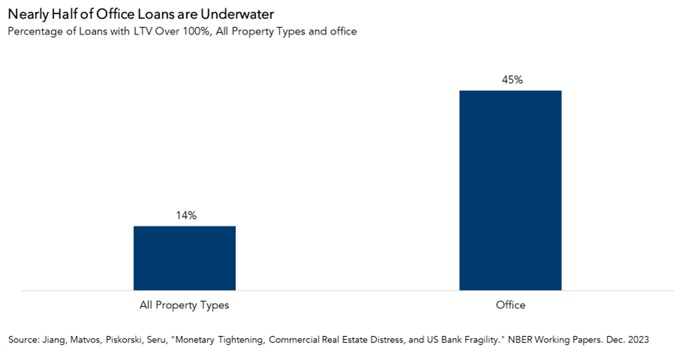

Measuring solvency requires estimates of property values for buildings that haven’t sold recently. These estimates are called appraised values, and a recent paper from the National Bureau of Economic Research (“NBER”) put a figure to how many CRE mortgages across all asset classes may be underwater based on appraised values. It found that 14 percent of all CRE loans may now be underwater, and likely almost 50 percent of office loans. Taken together, these high measures of illiquidity and insolvency indicate that the risk of foreclosure within the office sector is greater than that of other CRE asset classes.

Necessary, but Insufficient

While distress is a concern that’s front of mind for many in the CRE industry this year, not all distress looks the same and not all distress leads to delinquency or foreclosure. An underwater mortgage won’t necessarily become delinquent as long as it is liquid. Having liquidity gives owners and lenders breathing room, which discourages foreclosures and makes it easier for lenders to work with borrowers to amend existing loan terms. Illiquidity and insolvency present different challenges for operators. Each “trigger” is necessary, but insufficient on its own to force foreclosure and it’s worth bearing this distinction in mind.