When most people think of a loan, they think of a bank. Banks take deposits from customers in return for interest payments or other services. The bank then invests those deposits in loans, such as commercial real estate (CRE) loans, and securities that pay a higher interest rate than the bank is paying on the deposits. However, a bank is not the only place a commercial property owner can get a loan. There are a number of nonbank lenders that don’t raise money through deposits, but are active lenders to the CRE market. This month’s X-Factor examines how active nonbank lenders are in the CRE lending market compared with banks.

“In today’s tight credit market, some nonbank lenders, especially those with higher risk tolerances, may be able to provide liquidity as traditional banks pull back from CRE lending.”

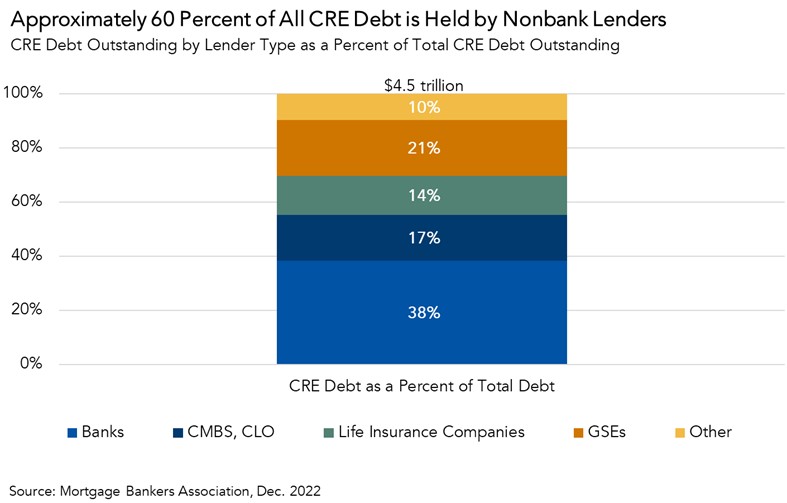

Most CRE Mortgages Are Held by Nonbank Lenders

There is approximately $4.5 trillion of CRE debt currently outstanding, yet only about $1.7 trillion of that amount is held by banks. The remaining $2.8 trillion is owned by nonbank lenders, which include life insurance companies, Government Sponsored Enterprises (GSE) – like Freddie Mac or Fannie Mae – mortgage REITs, and private debt funds, or is held as securitized commercial debt such as Commercial Mortgage Backed Securities (CMBS) or Collateralized Loan Obligations (CLOs). Nonbanks account for a greater share of lending for most asset classes, though the nonbank share is largest in multifamily lending at about 70 percent. This large nonbank lender share is due to the presence of the GSEs in residential real estate markets, as they regularly purchase and hold residential mortgages originated by other lenders, including mortgages for apartment buildings.

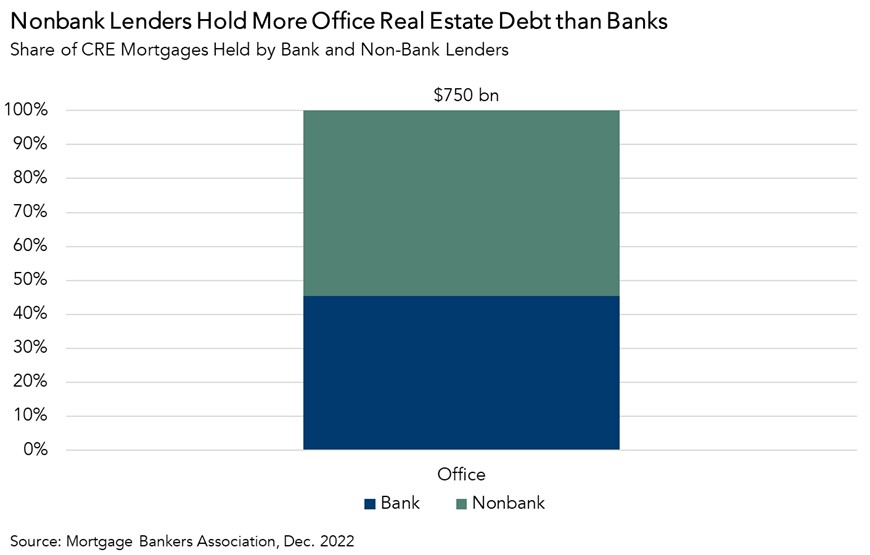

Banks Hold Slightly Less Than Half of All Office Property Debt

Office property loans comprise approximately 17 percent, or $750 billion of the $4.5 trillion in total CRE debt. Approximately 45 percent of these office loans are held by banks, with the remaining 55 percent held by nonbanks.

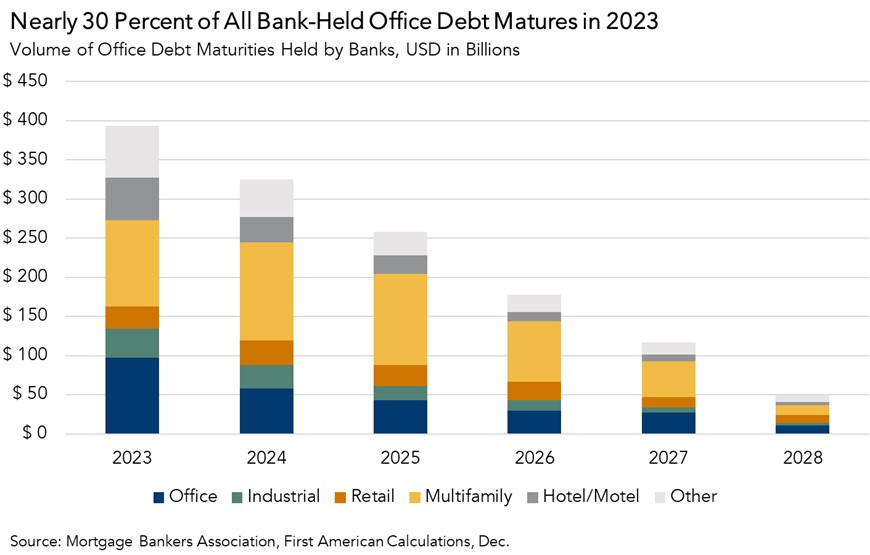

Substantial Portion of Bank-Held Office Loans Mature in 2023 and 2024

Nearly 30 percent of bank-held office debt, approximately $98 billion, will mature in 2023 alone. With office space utilization substantially below pre-pandemic levels, and interest rates much higher, many are concerned that the new financing available to some of these buildings will not be covered by the cash flow they generate. That raises the question of what banks will do if they currently hold the mortgage against a difficult-to-refinance building. However, these maturing office loans only account for approximately 6 percent of all bank-held CRE debt when including other asset classes.

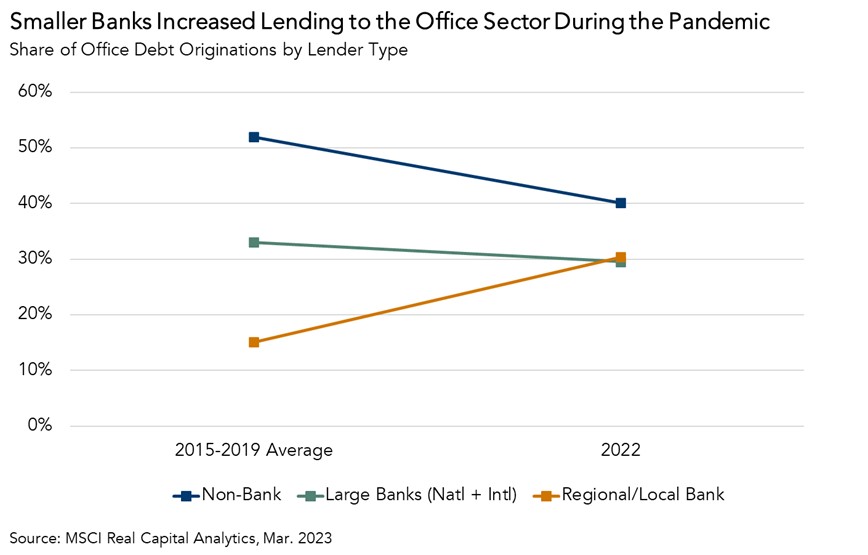

Smaller Banks Gained Market Share During Pandemic

While smaller banks provided more lending to the CRE market during the pandemic, in total they currently hold slightly less than one-third of all outstanding CRE debt.

So, What’s the X-Factor?

Nonbank lenders make up a substantial portion of the CRE lending market. While the bank side of this market has attracted the most attention, more than half of all CRE mortgages outstanding are held by nonbank lenders. In the wake of the recent bank failures, many are expecting greater regulatory scrutiny for banks of all sizes. In today’s tight credit market, some nonbank lenders, especially those with higher risk tolerances, may be able to provide liquidity as traditional banks pull back from CRE lending.