The first quarter of 2026 presented a markedly different environment from the strong and broadly supportive backdrop that characterized much of 2025 and the early part of 2026. Financial markets entered the year with constructive momentum, supported by resilient economic data, solid corporate earnings, and expectations for a continued easing cycle in monetary policy. However, as the quarter progressed, the positive narrative was flipped as conflict in the Middle East triggered a sharp reversal of previous expectations for moderately declining inflation and a measured path of additional interest rate cuts this year.

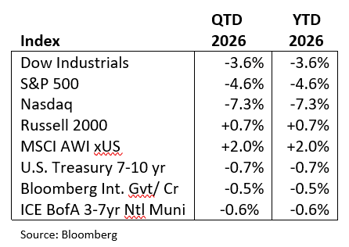

U.S. equity markets declined over the period, with the S&P 500 falling 4.6%, the Dow Jones Industrial Average declining 3.6%, and the Nasdaq Composite losing 7.3%, while small-cap equities were modestly positive. The quarter was defined by a sharp inflection in sentiment following the late February U.S. – Israel attack on Iran which led to a significant rise in energy prices and a corresponding shift in inflation expectations. This development disrupted the prevailing narrative of steady disinflation and monetary easing, introducing renewed uncertainty around both the economic outlook and the policy path.

Despite market volatility, underlying economic data for much of the quarter continued to reflect a fundamentally resilient, though increasingly uneven, U.S. economy. Early indicators pointed to steady growth across manufacturing and services, supported by stable consumer activity and a still-healthy labor market. As the quarter progressed, however, signs of strain became more evident. Employment data grew more volatile, housing activity softened under the weight of affordability pressures, and inflation measures began to reaccelerate, even prior to the impact of higher energy prices. By quarter end, the combination of moderating growth and rising price pressures raised concerns that the economy could be entering a more challenging phase. March data, to be released over the next several weeks, is now forecast to show a marked deterioration in both the growth and inflation outlooks as well as in numerous other key economic indicators.

Monetary policy expectations have already adjusted significantly in response. At the start of the year, markets anticipated a gradual series of rate cuts beginning mid-year. By the end of the quarter, those expectations had largely dissipated, as persistent inflation and geopolitical risks led investors to consider the possibility that policy could remain restrictive for longer or potentially even see rates rise. The Federal Reserve at its March policymaking meeting, maintained a cautious stance, holding rates steady while signaling a heightened sensitivity to inflation risks.

At the sector level, market leadership shifted meaningfully. Commodity-oriented sectors such as Energy and Materials benefited from sharply rising prices due to the Iran war, while more defensive areas of the market also held up relatively well amid heightened uncertainty. In contrast, several of the sectors that had driven market leadership in prior periods, including Technology, Financials, and Consumer Discretionary, lagged during the quarter. Beneath the index level, dispersion increased as investors placed greater emphasis on company-specific fundamentals, capital allocation decisions, and the sustainability of growth expectations, particularly in areas tied to AI and related capital investment. Rotational dynamics were also evident in style factor performance during the quarter as the typically defensive high dividend yield factor was the best performer, rising 3.8%, while the growth style factor was the worst performer, falling 9.8%.

Corporate earnings results for the fourth quarter of 2025, released during the first three months of the year, were generally solid, but forward guidance reflected a more cautious tone across a broad range of industries. While demand trends remained stable in many areas, companies increasingly cited margin pressures from higher labor, input, and financing costs, as well as uncertainty related to the macroeconomic and geopolitical environment. This dynamic was particularly evident in consumer-facing sectors, where spending remained intact but increasingly focused on value. We expect Q1-2026 earnings season to be more volatile, as companies highlight the impact of the first month of the war on their business models and financials, and assess the ramifications of ongoing uncertainty tied to the conflict. We note that although analyst estimates for first quarter earnings have declined modestly, full-year forecasts still point to higher earnings growth than last year and do not seem to have been adjusted for the potential of slower economic growth, higher inflation and further moderation in consumer spending.

Fixed income markets also reflected the evolving macro backdrop. Treasury yields moved higher over the quarter, with the 10-year yield rising to 4.32%, as inflation expectations increased and the anticipated path of monetary policy shifted. While some securitized sectors posted slight positive returns, Treasury bonds, as well as investment grade corporate and high yield bonds were modestly negative as rates moved higher and markets repriced expectations for inflation, growth, and Federal Reserve policy. Even with this quarter’s consolidation, yields remain attractive by historical standards and continue to provide a solid base of income.

Looking ahead, we expect the balance of 2026 to be shaped by elevated geopolitical uncertainty and the risk that the conflict in the Middle East results in a more persistent energy shock, pushing inflation higher while weighing on growth. Weaker labor markets and the current level of interest rates may temper the risk of a sustained, rather than transitory, rise in inflation, but the Federal Reserve still faces a difficult trade-off between looking through a supply-driven inflation impulse and responding if underlying demand begins to soften. While this backdrop may delay or complicate the path of rate cuts, it also reinforces the value of high-quality bonds as a source of income, diversification, and resilience.

Within fixed income portfolios, we remain selective, emphasizing liquidity, resilience, and credit quality. U.S. government-guaranteed mortgage securities (Agency MBS) continue to offer attractive relative value, with spreads over Treasuries still elevated relative to historical norms, making them a compelling alternative to corporate credit. While credit fundamentals remain generally sound, tight spreads limit compensation for incremental risk, making careful sector and security selection essential in 2026. International fixed income also presents meaningful opportunities as growth, inflation, and policy paths diverge across regions, enhancing the diversification benefits of less synchronized global cycles. As always, duration should align with client cash flow needs and remain anchored near neutral levels, with intermediate maturities offering an attractive balance of income, risk management, and total return potential.

International equities continued to outperform during the quarter, but that was primarily a function of strong performance in January and February as the asset class lagged in March as the war against Iran escalated. Economic dislocation from the war highlighted the vulnerabilities of key markets, particularly in W. Europe, Japan and select emerging markets, to much higher energy prices and supply shortages as well as the derivative impacts on food prices and manufacturing inputs. As in the U.S., the expected increase in inflation has forced central banks to reconsider previous rate-cutting plans, thus putting economic growth forecasts in jeopardy. We continue to monitor these markets closely for signs of a clear breakdown relative to U.S. equity markets.

The remainder of 2026 clearly presents a less uniformly supportive backdrop than previously expected as geopolitical risk, inflation uncertainty, and policy constraints are certain to play a more prominent role. Within equities, these conditions reinforce the importance of maintaining a disciplined and balanced approach. Increased volatility and dispersion across sectors and securities create both risks and opportunities, underscoring the value of active management and careful security selection. We continue to emphasize high-quality businesses with durable competitive advantages, strong balance sheets, and the ability to navigate a range of economic environments. Ongoing shifts in market leadership remains an important theme, although near-term performance may continue to be influenced by macroeconomic developments and investor sentiment.

Finally, we note that while the near-term outlook has become more uncertain, the underlying foundations of the economy remain intact. The adjustment currently underway appears less indicative of a fundamental deterioration and more reflective of a repricing of risks and expectations following an extended period of strong returns. As such, we believe a focus on quality, diversification, and long-term fundamentals remains the most effective approach to navigating the current environment and positioning portfolios for sustainable returns over time.

Author:

|

Bruce Schoenfeld, CAIA® Principal Investment Analyst First American Trust |

Bruce is the Principal Investment Analyst responsible for investment research coverage of various asset classes and equity industry sectors. Bruce has more than 27 years of experience as an equity analyst and portfolio manager. He joined First American from 3P Associates, LLC, an investment and strategic management consulting firm he founded. He previously served as Director of Research at BlueStar Global Investors and as an analyst and portfolio manager focused on emerging markets for Delaware Investments, Artha Capital and Caisse de depot et placement du Quebec, Canada’s second largest pension fund.

Co-Authors: |

Jason Nerio SVP, Director of Investment Research & Strategy First American Trust |

Jason Nerio is the Director of Investment Research and Strategy at First American Trust. Mr. Nerio has more than 28 years of investment research experience. He is responsible for formulating investment strategy and serves as a leading member of the investment committee which monitors and manages the firm’s allocation strategies for over $2 billion in client assets.

|

Scott Dudgeon, CFA® Director, Equity Research First American Trust |

Scott Dudgeon is the Director of Equity Research at First American Trust. Mr. Dudgeon is a Chartered Financial Analyst® (CFA®) Charterholder and has more than 29 years of investment research experience. He also serves as a leading member of the investment committee and has a proven track record for outperforming the markets for our clients. He has been with The First American Family of Companies for 20+ years.

The following article is for informational purposes only and is not and may not be construed as legal and/or investment advice. Investments contain risks, no third-party entity may rely upon anything contained herein when making legal and/or investment determinations regarding its practices, and such third party should consult with an attorney and/or an investment professional prior to embarking upon any specific course of action.

Past performance is no guarantee of future results. Individual account performance will vary. Not FDIC insured. No Bank guarantee. May lose value.