One of the biggest market shifts in recent years is the resurgence of elevated inflation. This risk is prompting investors to pay closer attention to how risk assets move together. This relationship is known as correlation, and it is not a steady one. It changes depending on the inflation environment, and that has real consequences for the traditional 60/40 portfolio (60% stocks, 40% bonds).

The 60/40 portfolio relies on diversification, with stocks contributing growth and bonds providing income with stability during stock declines. This relationship works best when stocks and bonds move in opposite directions, which is called negative correlation.

An inflation environment is generally viewed as low when inflation remains below roughly 2.0%–2.5%. Below this range, the economic condition is considered calmer and more predictable. Economic growth is typically steadier, inflation expectations are stable, and central banks can cut interest rates to support growth if economic conditions deteriorate. When equity markets come under pressure in that kind of environment, investors often move quickly to price in an easier policy stance. Bond yields fall, bond prices rise, and bonds help reduce the impact of stock losses.

This relationship underpins the historical performance of the 60/40 portfolio in low inflation environments. The negative correlation between stocks and bonds acts as a stabilizing factor, leading to smoother returns and improved risk-adjusted performance.

The picture changes once inflation moves meaningfully above the 2.5% level. In that environment, the traditional relationship between stocks and bonds can start to break down. Central banks lose flexibility in an inflationary environment. Rather than cutting rates to support growth, they may have to maintain tight policy or even tighten further to bring inflation under control. If economic growth slows while inflation rises, both stocks and bonds can fall at the same time. Higher inflation drives up interest rates, which in turn lowers bond prices. Higher rates tend to compress equity valuations, while weaker economic activity weighs on corporate earnings. When stocks and bonds decline together, their correlation turns positive, and the diversification benefit that investors usually rely on begins to disappear.

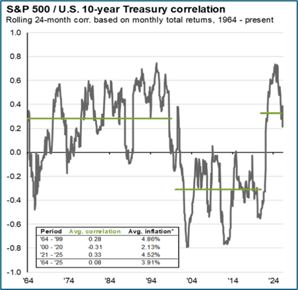

Historical analysis since 1964 from JP Morgan reveals that the stock and bond correlation is regime dependent. From the mid-1960s to 1999, when inflation averaged 4.86%, the correlation was generally positive. The relationship changed between 2000 and 2020, with the average inflation rate falling to 2.13% and the correlation turning negative, enhancing diversification. Since 2021, inflation has averaged 4.52%, and the correlation has reverted to positive, mirroring earlier inflation sensitive periods.

Over the last year inflation has been trending near the 2.5% borderline. Looking forward, however, there are growing reasons to think the market may be entering another elevated inflation phase. The US/Israel-Iran war appears to have affected key energy infrastructure and pushed oil prices higher. Rising energy costs tend to spread across the wider global economy. Businesses then face higher production, transportation, and supply chain costs. Those higher costs are often passed on to consumers. The result can be broader upward pressure on prices and a rise in overall inflation.

If this happens, central banks might have to keep tight monetary policies in place longer than expected. In this environment, the correlation between stocks and bonds usually rises, making things tougher for traditional portfolios.

When inflation becomes a primary concern, it is prudent to allocate to assets that either benefit from inflation or are less negatively impacted by it. We believe that real assets, including commodities, energy, and infrastructure, function as effective portfolio diversifiers. International assets and Treasury Inflation-Protected Securities can also function as valuable inflation hedges.

- Commodities are especially effective because they tend to respond rapidly to inflation, especially when driven by supply disruptions. Their performance often aligns with inflation trends, offering diversification benefits when both equities and bonds underperform.

- Energy exposure is especially relevant now. When inflation is driven by rising energy prices, these assets can experience revenue and margin expansion, offsetting losses elsewhere in the portfolio, providing a natural hedge.

- Infrastructure investments can be a good hedge. They are typically regulated or supported by contracted revenue streams that frequently incorporate inflation pass-through mechanisms. These features enable cash flows to rise with price levels, offering stability and preserving real returns during inflationary periods.

- International stocks and bonds can also improve diversification, as inflation shocks vary across regions. Select economies, particularly commodity exporters, can benefit from rising prices, creating opportunities in non-U.S. equities, currencies, and sovereign bonds.

- Inflation-linked bonds - Their principal adjusts with inflation, helping to preserve real purchasing power.

The traditional 60/40 portfolio is still a strong approach, but how well it works depends on the current inflation environment. In times of low inflation, stocks and bonds usually move in opposite directions, which helps with diversification. When inflation moves above 2.5%, correlations can turn positive, reducing the benefits of diversification.

With inflation risks possibly rising again, it makes sense to review how your portfolio is built. Adding real assets such as commodities, infrastructure, and energy stocks brings in investments that benefit from inflation. International exposure gives access to regions that might gain from higher prices, and inflation-linked bonds help protect your purchasing power. Including these assets can boost diversification and make your portfolio stronger during inflationary periods.

In recent quarters, First American Trust has taken steps to position portfolios to address a broader range of inflationary conditions by integrating some of these inflation beneficiaries. Our aim is to improve resilience while maintaining flexibility as market conditions change. We welcome further discussion regarding how these areas can support your portfolio objectives. Please contact your relationship manager for additional information.

Author:

|

Jason Nerio Senior Vice President, SVP, Director of Investment Research & Strategy First American Trust |

Jason Nerio is the Director of Investment Research and Strategy at First American Trust. Mr. Nerio has more than 28 years of investment research experience. He is responsible for formulating investment strategy and serves as a leading member of the investment committee which monitors and manages the firm’s allocation strategies for over $2 billion in client assets.

The following article is for informational purposes only and is not and may not be construed as legal, tax and/or investment advice. Investments contain risks, no third-party entity may rely upon anything contained herein when making legal, tax and/or investment determinations regarding its practices, and such third party should consult with an attorney, tax advisor and/or an investment professional prior to embarking upon any specific course of action.

Past performance is no guarantee of future results. Individual account performance will vary. Not FDIC insured. No Bank guarantee. May lose value.