If you own an investment property and are looking to sell, you may want to consider a 1031 tax-deferred exchange. This wealth-building tool can help you sell one investment property and purchase another while deferring taxes, including federal capital gains taxes, state capital gains taxes, the recapture of depreciation and the newly implemented 3.8% Medicare Tax, which can significantly increase your buying power.

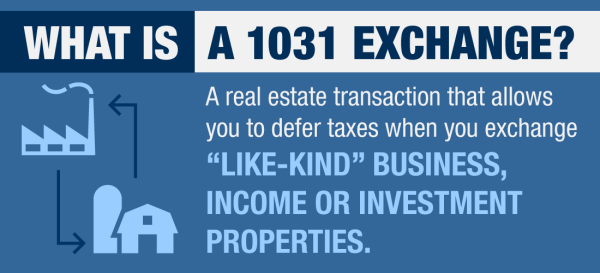

What is a 1031 exchange?

Section 1031 of the IRC falls under the headline Like-Kind Exchanges. It involves exchanging real estate properties of "like-kind" in order to defer numerous taxes.

Basically, if you own a property for productive use in a trade or business - in other words, an investment or income-producing property - and want to sell it, you have to pay various taxes on the sale. This tax burden means that you'll be left with much less money if you choose to use the proceeds of the sale to buy a replacement property. Because you're selling one property in order to replace it with another investment property, this loss of money to the various taxes due can seem frustrating.

Fortunately, this is where the 1031 exchange comes in to play. This transaction allows you to exchange your investment or income-producing property for another that is "like-kind." As long as the real estate is in the United States and used in business or held for income or investment, it is considered like-kind. By using this method, you can defer paying several tax liabilities.

Eligibility requirements

As mentioned, a 1031 exchange is reserved for property held for productive use in a trade or business or for investment. This means that any real property held for investment purposes can qualify for 1031 treatment, such as an apartment building, a vacant lot, a commercial building, or even a single-family residence. It is important to note that property held primarily for personal use does not qualify for tax-deferral under Section 1031. This would include a primary residence and a second home. In some situations, a taxpayer can exchange a vacation home as long as that taxpayer had limited personal use of the property. However, a 1031 exchange is not restricted to real estate alone. Some personal property may qualify for a 1031 exchange too.

The IRS has created a list of who qualifies for this exchange:

- Individuals

- C corporations

- S corporations

- Partnerships (general or limited)

- Limited liability companies

- Trusts

- Any other taxpaying entity

In this way, the regulations surrounding who can perform the exchange and what can be exchanged are fairly broad, but there are time restrictions for a 1031 exchange. The replacement property must be identified within 45 calendar days of closing the sale of the first property. Furthermore, you are only allowed to have 180 calendar days between the close of your first property's sale and the close of the replacement property's purchase. To conduct a 1031 exchange, the IRS requires you to use the help of a Qualified Intermediary – like First American Exchange Company – to oversee the transaction and ensure that all exchange requirements are met.