The Real Estate Settlement Procedures Act requires a mortgage lender to issue a Good Faith Estimate to all potential borrowers. When you apply for a mortgage, make sure you receive this form from your lender.

What is the Good Faith Estimate?

The GFE is a standardized form you should receive from your lender after applying for a mortgage. It provides you with an estimate of the settlement charges and loan terms you'll likely have if you're approved for the loan. For example, on this form, you'll find the loan's term and initial interest rate, in addition to whether your loan balance can rise even if you make payments on time.

It's a good idea to shop around for the best loan terms, so utilize your GFEs to compare different options. However, it's important to note that the GFE is merely an estimate. It does not provide secure, definite terms, so don't fully rely on the numbers it provides. Fortunately, the government has instituted tolerance levels, which designate how much each GFE figure can increase at closing. This should minimize the surprises at settlement.

Tolerance levels break the GFE figures up into three categories: those that cannot increase at closing (also considered a zero percent tolerance level), those that can increase up to 10 percent at closing and those that can change in any amount at closing (considered to have no tolerance level). These restrictions are intended to help protect consumers and create more transparency in the lending process.

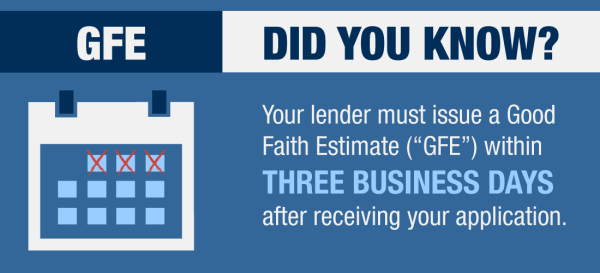

Know your rights: The three-day rule

One thing many people may not know about the Good Faith Estimate is that your lender is legally required to provide it within three business days of receiving your mortgage application. If you don't receive your GFE in that time, the lender may be in breach of federal law. However, it's also important to note that if your loan application is denied before the end of the three-day period, the lender isn't required to provide a GFE.

In addition, the law states that the lender must provide the GFE after receiving a completed loan application, and there is a specific definition of what constitutes a complete application. It must include the following:

- Borrower's name;

- Borrower's monthly income;

- Borrower's social security number;

- Property address;

- Estimated value of the property;

- Loan amount; and

- Anything else the lender may deem necessary

If your loan application was not complete under these criteria, the lender is not required to give you a GFE. With this in mind, make sure you are thorough with your application and are providing everything necessary to be granted a GFE.