Last week, the Federal Open Market Committee (FOMC) met for the second to last time this year. As most prognosticators expected, the FOMC decided to leave the short-term Federal Funds rate unchanged. While good news for those with credit card debt, car loans and adjustable rate mortgages, the impact of FOMC inaction, or action for that matter, is less clear for the mortgage market. Additionally, Jerome Powell was nominated to be the next Chairman of the Federal Reserve and he is widely believed to hold a similar stance on monetary policy as the current chair, Janet Yellen.

As I noted preceding the FOMC meeting in September, the short-term Federal Funds rate has no impact on the majority of existing-home owners, currently more than half of all households in the U.S., because they have 30-year, fixed-rate mortgages. The operative words being 30-year and fixed in that statement. Thirty-year fixed-rate mortgages are influenced by long-term rates, little impacted by short-term FOMC action or inaction. If it’s a fixed rate mortgage it is, by design, unchangeable by movements in the market rate.

The more relevant question is, at what mortgage rate do homes become unaffordable for the other 36.1 percent of households (according to most recent Census estimate of the homeownership rate), who are not homeowners and who potentially would like to buy their first home?

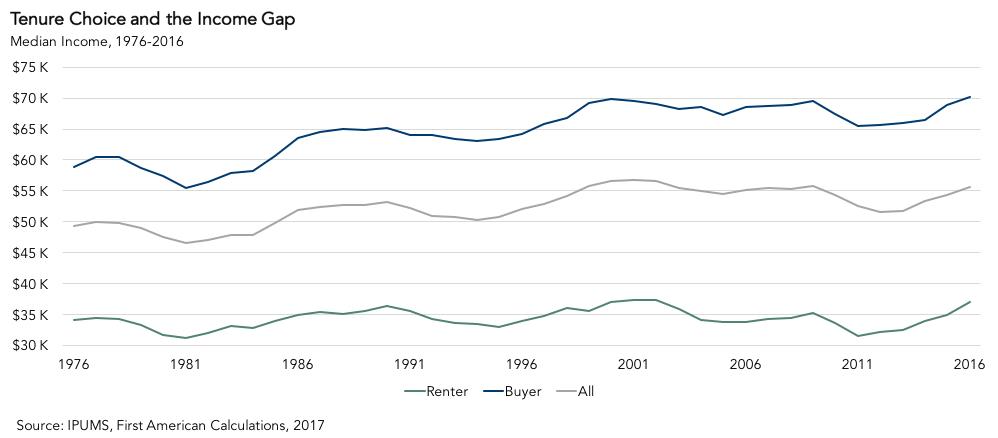

Of course, the answer to this question will vary based on where you live, the price of homes in that market and how much income you can afford to spend on a mortgage payment. Many experts use the median household income of all households to analyze this question, but that overlooks the differences in income levels between the typical homeowners and the typical renter.

Not surprisingly, homeowner households have higher household incomes than renter households. In fact, as of the latest 2016 Census data, the median annual income for homeowner households is $70,000 and the median annual income for renter households is $37,000. So, the income gap between homeowners and renters is $33,000. So, using the median household income for all households, $56,000, will inflate the estimate of what a typical renter and potential first-time home buyer can reasonably afford to borrow.

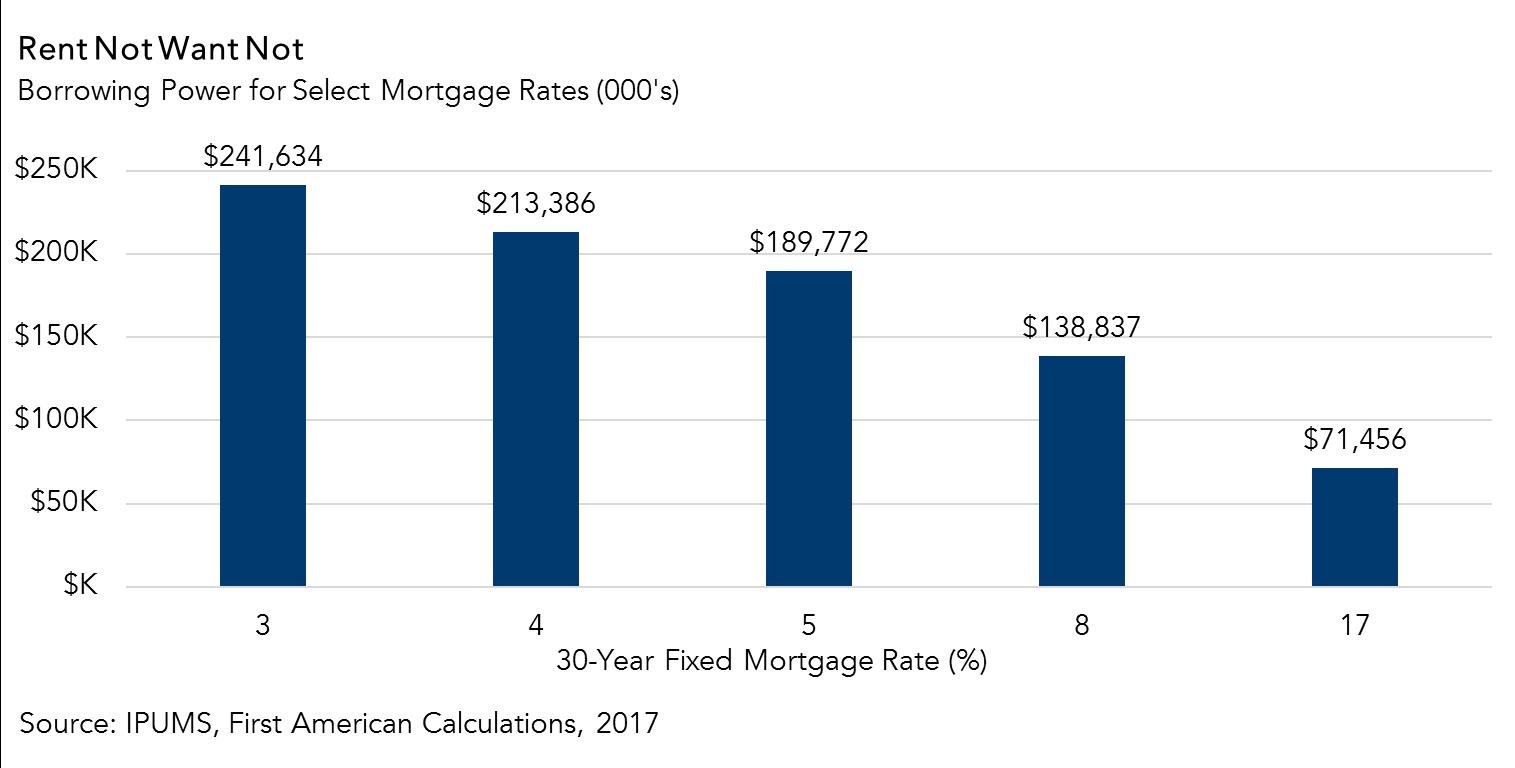

Instead, let’s focus on the mortgage principal and interest payment that would be reasonable for the typical renter to afford and how that might change as rates change. The figure below uses the median rental household income in 2016 of $37,000 and assumes that one-third of the renter’s gross monthly pay can be spent on a mortgage.

The current 30-year, fixed mortgage rate is approximately 4 percent and, given the renter’s income, they can borrow $213,000. The lowest 30-year, fixed-rate mortgage in over 40 years was about 3 percent in 2012. At that mortgage rate, our renter could have borrowed $242,000, 13 percent more than at today’s rate. For the sake of comparison, at the highest mortgage rate in the last 40 years, 17 percent in 1981, our renter could only afford to borrow $71,000, 67 percent less than at today’s rate. Looking ahead, if the 30-year, fixed-rate mortgage rises to approximately 5 percent, which is the consensus among economists for the end of 2018, then our renter can borrow $190,000, which is still well above the long-run average of $139,000 at a mortgage rate of 8 percent.

While borrowing power for the potential home buyer has fallen relative to the low point of 2012, it remains high today and will remain high next year, relative to the long run average. If you don’t want to rent anymore and are considering becoming a homeowner, even if mortgage rates rise next year, your borrowing power will remain strong by historic standards. Because real estate is, after all, local, stay tuned for an analysis of borrowing power for rental households by geography.