It’s a near certainty that the Federal Open Market Committee (FOMC) will raise the short-term Federal Funds rate this week. The CME group estimates the probability of a 25 basis-point increase at 90.2 percent. Some may fret about how this will impact the housing market, but they are missing the point on mortgage rates and affordability for first-time home buyers.

It’s important to remember that a change in the short-term Federal Funds rate has no impact on the majority of existing homeowners, as most have 30-year, fixed-rate mortgages. Thirty-year, fixed-rate mortgage rates are more strongly influenced by long-term rates. Short-term FOMC action or inaction has little impact on the interest rates for 30-year, fixed rate mortgages.

“It is easy to overlook, but the reality is renters have greater borrowing power today than in most of the last 40 years and that won’t change, even as mortgage rates rise in 2018.”

However, it’s a different story for renters, which make up 36.1 percent of households according to the most recent Census estimate of the homeownership rate. For those renters that are potential home buyers, any influence that a short-term rate change has on mortgage rates can be materially consequential to how much they can afford to buy.

Last month, we examined the borrowing power for households making the median annual household income nationally for renters ($37,000) at different mortgage rates. But, as the old adage goes, real estate is local, and so are income levels, which vary substantially across the country.

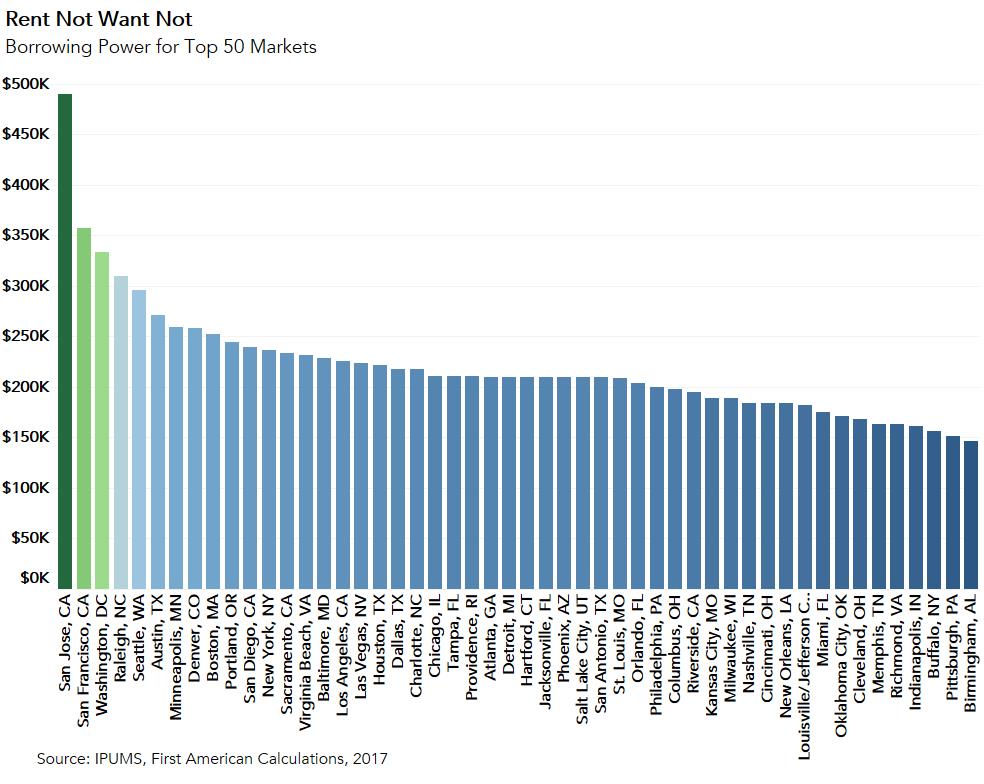

For example, of the top fifty largest markets analyzed, San Jose, Calif. has the highest median annual renter household income of approximately $91,000, followed by San Francisco ($66,000), Washington, D.C. ($62,000), Raleigh, N.C. ($57,000), and Seattle ($55,000). So, which cities offer first-time home buyers the most borrowing power?

Using each market’s annual median renter household income, assuming that a household spends one-third of their gross monthly pay on a mortgage, and that a 30-year, fixed-rate mortgage rate is 5 percent (consensus forecast among economists for the end of 2018), the five cities where renters have the most borrowing power are:

- San Jose, CA: $490,143

- San Francisco, CA: $357,465

- Washington, DC: $333,652

- Raleigh, NC: $310,007

- Seattle, WA: $295,750

The five markets where renters have the least borrowing power are:

- Birmingham, AL: $146,140

- Pittsburgh, PA: $151,917

- Buffalo, NY: $156,375

- Indianapolis, IN: $161,490

- Richmond, VA: $162,967

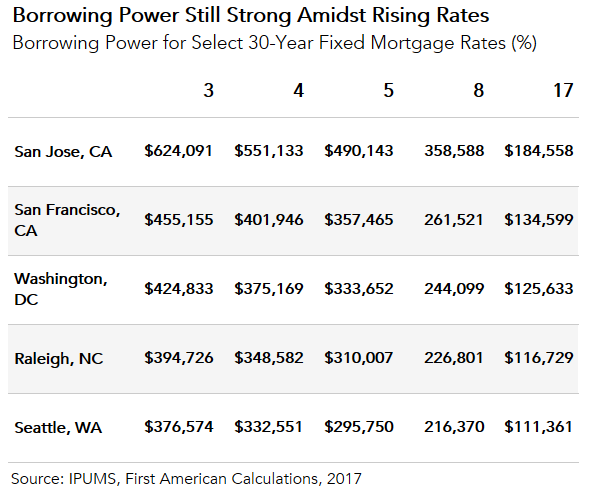

To demonstrate how sensitive borrowing power is to changes in mortgage rates, the chart below indicates how much a rental household could borrow in the top markets at a variety of different mortgage rates. Each different mortgage rate provides some historical perspective -- from the lowest mortgage rate in 40 years of 3 percent in 2012, today’s rate of 4 percent, the consensus forecast rate for end of 2018 of 5 percent, the long-run average rate of 8 percent, and 17 percent, which was the mortgage rate in 1981 and the highest mortgage rate in the past 40 years.

While borrowing power has fallen marginally for the potential home buyer relative to the lower 30-year, fixed mortgage rate of 3 percent in 2012, it remains higher across all markets compared to the long-run historical average mortgage rate. It is easy to overlook, but the reality is first-time home buyers have greater borrowing power today than in most of the last 40 years and that won’t change, even as mortgage rates rise in 2018. So, fear not, potential first-time home buyers, the American Dream will remain within reach if mortgage rates rise next year.

Odeta Kushi contributed to the blog post.